Stocks vs Bonds: Which Is Better for Beginner American Investors in 2026?

Stocks vs Bonds: Which Is Better for Beginner American Investors in 2026?

Confused between stocks and bonds? Learn the key differences, risks, returns, and best strategies for beginner American investors with simple US examples.

Stocks vs Bonds: A Simple Guide for Beginner American Investors

If you are new to investing, one big question comes up quickly:

Should I invest in stocks or bonds?

Both are popular. Both can grow your money. But they behave very differently.

In this beginner-friendly guide, we’ll clearly explain:

What stocks are

What bonds are

Risk vs return differences

Real US examples

How to decide what fits you

Let’s make it simple and practical.

What Are Stocks?

New York Stock Exchange trading floor

Beginner checking stock market app USA

Rising stock market chart example

Long term stock investing concept

When you buy a stock, you buy a small piece of ownership in a company.

For example:

If you purchase shares of Apple Inc., you become a part-owner of that company.

If the company grows:

The stock price may rise

You may receive dividends

If the company struggles:

The stock price may fall

Stocks offer higher growth potential, but they also move up and down daily.

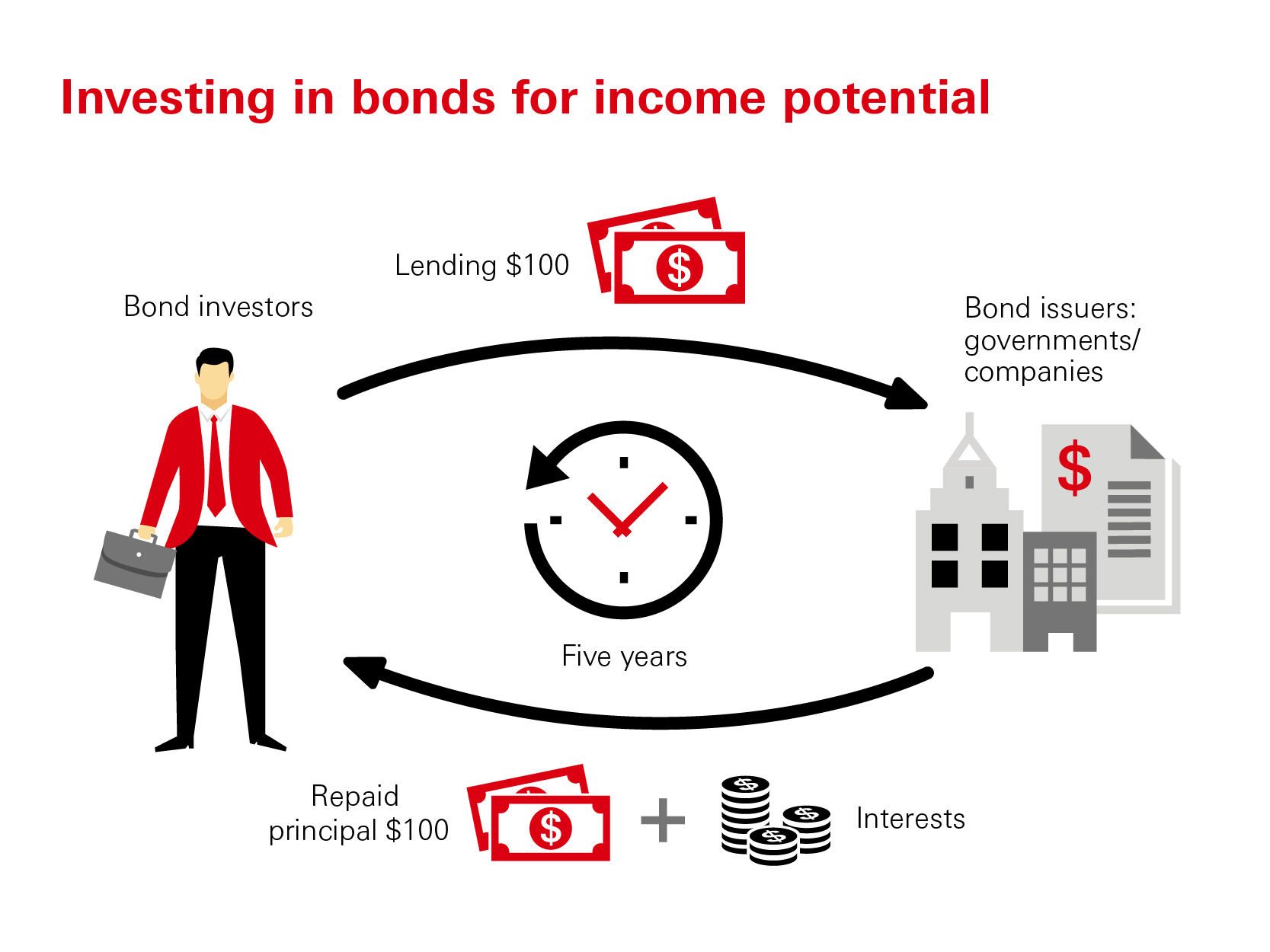

What Are Bonds?

Image ALT Tags:

US Treasury bond certificate example

Government bond investment USA

Fixed income bond concept

Bond interest payment illustration

When you buy a bond, you are lending money.

For example:

Buying a U.S. Treasury bond means you are lending money to the U.S. government.

In return:

You receive regular interest payments

You get your principal back at maturity

Bonds are generally considered safer than stocks, but they usually grow more slowly.

Key Difference: Ownership vs Lending

| Feature | Stocks | Bonds |

|---|---|---|

| What you own | Part of a company | Loan agreement |

| Risk level | Higher | Lower |

| Return potential | Higher long-term | Moderate |

| Income | Dividends (not guaranteed) | Fixed interest payments |

| Price movement | More volatile | More stable |

Chart: Historical Average Returns

Investment Type | Average Annual Return (Long-Term)

-------------------------------------------------------------

US Stocks (S&P 500) | ~8–10%

US Treasury Bonds | ~3–5%

Savings Account | ~0.5–1%

Historical averages, not guaranteed future results.

For stock performance tracking, many investors follow the S&P 500.

Risk: What Beginner Investors Must Understand

Stocks can drop 20–30% during market corrections.

Bonds usually fall less during downturns.

Example:

During major market downturns, stock investors may panic and sell at losses. Bond investors usually see smaller declines.

But remember — higher risk often brings higher reward over long periods.

Real-Life US Example

Let’s say:

Emily, age 30, invests $10,000 in stocks.

Michael, age 60, invests $10,000 in bonds.

Emily:

Has 30+ years before retirement

Can handle ups and downs

Seeks long-term growth

Michael:

Is close to retirement

Wants stability

Prefers predictable income

Both choices are correct — for their situation.

When Stocks May Be Better

Stocks may suit you if:

You are young (20s–40s)

You have stable income

You can invest long-term (5+ years)

You can handle short-term market drops

You want higher growth

If you are just starting, read our detailed guide on “What Is Investing? A Beginner’s Guide for Americans” (Internal Link).

When Bonds May Be Better

Bonds may suit you if:

You are near retirement

You need steady income

You dislike market volatility

You want capital preservation

Bonds reduce overall portfolio swings.

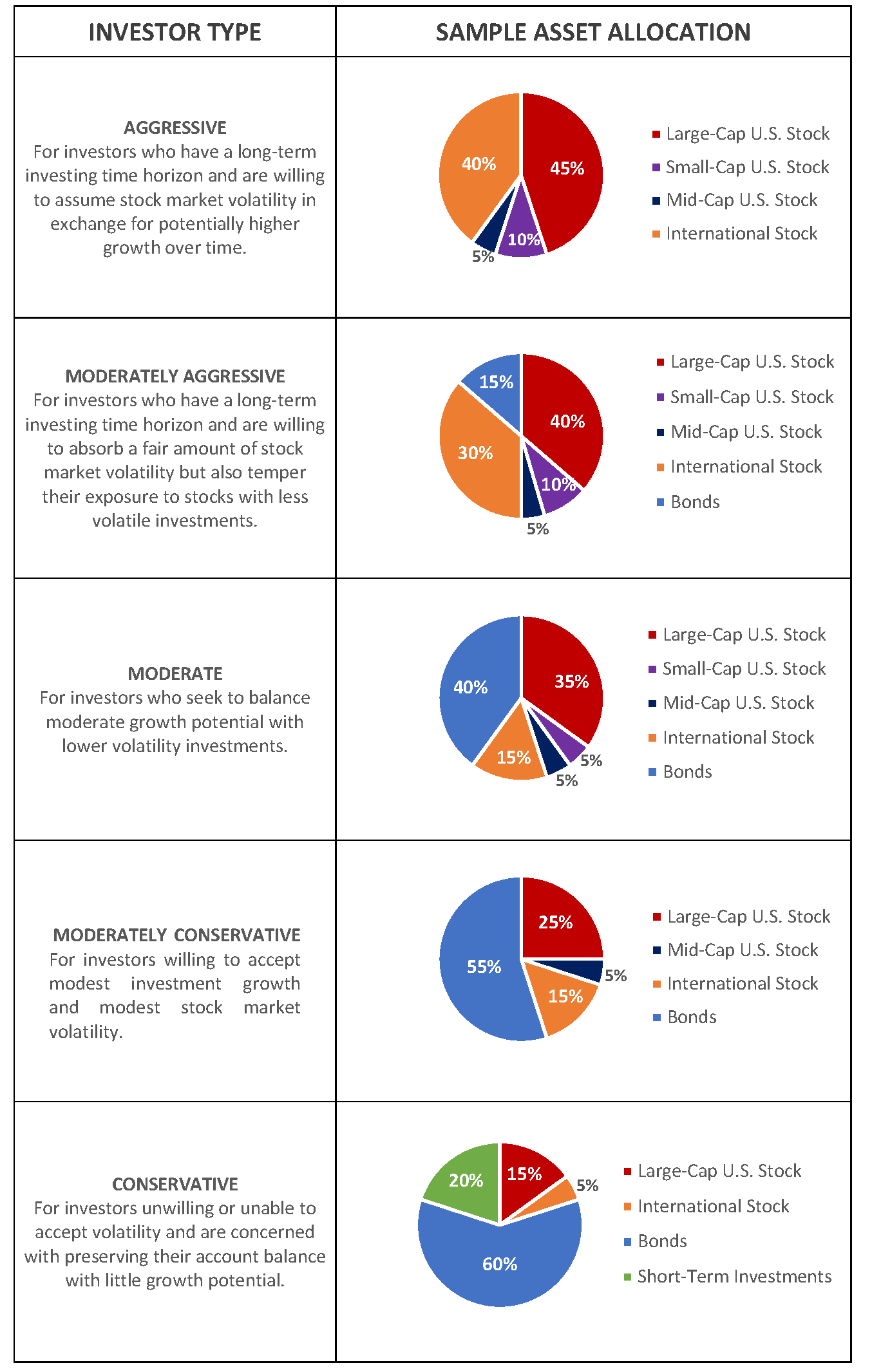

The Smart Answer: Why Not Both?

Diversified investment portfolio example

Asset allocation stocks and bonds pie chart

Retirement portfolio mix example

Financial planning discussion USA

Most financial advisors recommend a mix of stocks and bonds. This is called asset allocation.

Simple beginner rule:

Younger investors: More stocks

Older investors: More bonds

Example allocation:

Age 30 → 80% stocks, 20% bonds

Age 50 → 60% stocks, 40% bonds

Age 65 → 40% stocks, 60% bonds

This balances growth and safety.

Simple Portfolio Flow Diagram

Start Investing

↓

Build Emergency Fund

↓

Contribute to 401(k)

↓

Choose Asset Allocation

↓

Invest in Stock ETFs

↓

Add Bond Funds for Stability

↓

Rebalance Every Year

If you haven’t built savings yet, first read our guide on “How to Build Emergency Savings in the USA” (Internal Link).

ETFs: The Beginner-Friendly Way

Instead of picking individual stocks or bonds, many beginners use ETFs.

For example:

Stock ETF tracking S&P 500

Bond ETF tracking US Treasury bonds

ETFs give instant diversification.

Taxes on Stocks vs Bonds

Stocks:

Capital gains tax when sold

Dividends taxed

Bonds:

Interest income taxed (except some municipal bonds)

Tax planning matters. To avoid errors, review our post on “Tax Mistakes Americans Make” (Internal Link).

Common Beginner Mistakes

Putting everything in one stock

Avoiding bonds completely

Panic selling during market drops

Ignoring fees

Trying to time the market

Long-term discipline matters more than perfect timing.

Risk vs Stability Visual Comparison

Market Ups & Downs

Stocks: ↑↓↑↓↓↑↑↓ (High fluctuation)

Bonds: ↑→↓→↑→↓ (Moderate movement)

Savings: →→→→→→ (Minimal change)

Official Educational Resources

Investor Education:

U.S. Securities and Exchange Commission – https://www.investor.gov

Financial Industry Regulatory Authority – https://www.finra.org

Market Data:

New York Stock Exchange – https://www.nyse.com

Educational Video:

FAQ

1. Are stocks better than bonds?

Not always. Stocks offer higher growth but higher risk. Bonds offer stability but lower growth.

2. Should beginners avoid stocks?

No. Young investors often benefit from stock exposure for long-term growth.

3. Can bonds lose money?

Yes, especially if interest rates rise. But usually less volatile than stocks.

4. What is a safe beginner strategy?

Diversified ETFs with both stock and bond exposure.

5. How often should I rebalance?

Once per year is generally sufficient.

Statutory Disclaimer

This article is for informational and educational purposes only. It does not constitute investment, financial, or tax advice. Investment markets involve risk, including loss of principal. Past performance does not guarantee future results. Please consult a licensed financial advisor before making investment decisions. moneysenseamerica.blogspot.com and the author are not responsible for financial decisions made based on this content.

Bibliography

U.S. Securities and Exchange Commission (SEC)

FINRA Investor Education Foundation

Federal Reserve Historical Data

S&P Dow Jones Indices Historical Reports

U.S. Department of the Treasury

Final Thoughts

Stocks grow wealth.

Bonds protect wealth.

For beginner American investors, the best approach is usually balance — not extremes.

Start small. Stay consistent. Think long-term.

If you want to build real financial confidence, explore more practical guides on moneysenseamerica.blogspot.com, including:

What Is Investing? A Beginner’s Guide for Americans

Tax Mistakes Americans Make

How to Build Emergency Savings in the USA

Your investing journey does not need to be complicated. It just needs to begin.

Comments

Post a Comment