How Much Life Insurance Do Americans Need? Simple Calculator, Examples & Expert Tips

How Much Life Insurance Do Americans Need? Explained Simply with Real Examples (2026 Guide)

How Much Life Insurance Do Americans Need? Simple Calculator, Examples & Expert Tips

Learn how much life insurance Americans really need. Use simple methods, real-life examples, charts, and smart tips to choose the right coverage for your family.

“American family planning life insurance coverage at home”

“Young parents reviewing life insurance needs in the USA”

“Couple calculating term life insurance amount together”

“Working adult using life insurance calculator online”

“Family budgeting with insurance and financial documents”

Many Americans buy life insurance.

But most of them ask later:

“Did I buy enough… or too little?”

Some people are underinsured.

Some people overpay.

Many people guess.

The truth is:

👉 There is a simple way to calculate how much life insurance you really need.

This guide explains everything in clear, practical language — with US examples, charts, and step-by-step methods.

Why Knowing the Right Coverage Amount Matters

Life insurance is not for you.

It is for:

✔ Your spouse

✔ Your children

✔ Your parents

✔ Anyone who depends on your income

If your coverage is too low → family struggles.

If it is too high → you waste money.

The right amount = protection + peace of mind.

Who Regulates Life Insurance in the US?

Life insurance is regulated and monitored by:

National Association of Insurance Commissioners

Internal Revenue Service

These agencies help ensure fair pricing, consumer protection, and tax rules.

What Does Life Insurance Actually Replace?

When you die, your income stops.

But your family still needs money for:

✔ Rent or mortgage

✔ Food and utilities

✔ School fees

✔ Healthcare

✔ Daily living

✔ Debt payments

Life insurance replaces your income when you are gone.

The 4 Most Common Coverage Mistakes

Before learning the right method, avoid these errors:

❌ Buying only employer insurance

❌ Choosing random round numbers

❌ Copying friends’ policies

❌ Ignoring future expenses

These mistakes leave families exposed.

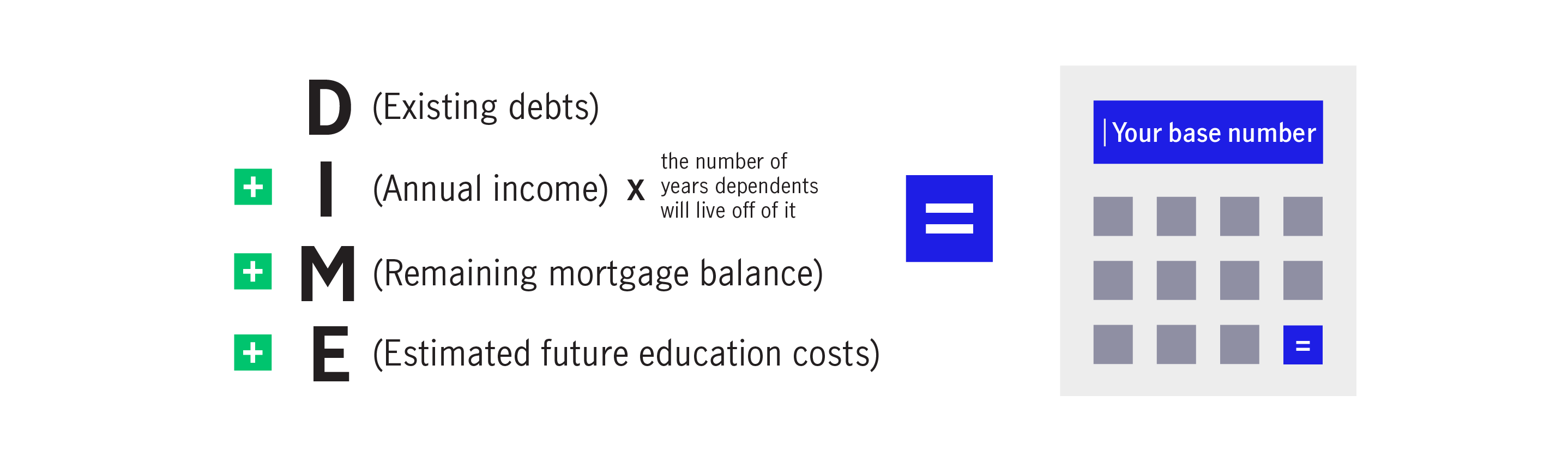

The Best Method: The DIME Formula (Simple & Powerful)

Financial planners often use the DIME Method.

It stands for:

| Letter | Meaning | Covers |

|---|---|---|

| D | Debts | Loans, cards |

| I | Income | Future income |

| M | Mortgage | Home loan |

| E | Education | Kids’ college |

Let’s break it down.

1️⃣ D — Debts

Add all unpaid debts:

✔ Credit cards

✔ Car loans

✔ Personal loans

✔ Medical bills

Example:

Credit cards: $8,000

Car loan: $12,000

Personal loan: $5,000

Total = $25,000

2️⃣ I — Income Replacement

This is the biggest part.

Ask:

“How many years should my family replace my income?”

Most experts suggest 8–12 years.

Example:

Annual income: $55,000

Years: 10

Income need = $550,000

3️⃣ M — Mortgage

Include your home loan balance.

Example:

Mortgage left = $190,000

This helps your family keep the house.

4️⃣ E — Education

Estimate children’s education cost.

Example:

Two kids × $50,000 = $100,000

Full DIME Example (Texas Family)

David — Truck Dispatcher, Dallas

Income: $58,000

Kids: 2

Mortgage: $210,000

Debts: $22,000

Calculation:

| Factor | Amount |

|---|---|

| Debts | $22,000 |

| Income (10 yrs) | $580,000 |

| Mortgage | $210,000 |

| Education | $100,000 |

| Total Need | $912,000 |

👉 Recommended coverage: $900k–$1M

Alternative Method: Income Multiple Rule

If you want a fast estimate, use:

Example

Income: $60,000

| Multiplier | Coverage |

|---|---|

| 10× | $600,000 |

| 12× | $720,000 |

| 15× | $900,000 |

Good for quick planning, but less accurate than DIME.

How Much Coverage Do Different Americans Need?

Single Adult (No Dependents)

| Situation | Suggested Cover |

|---|---|

| No debts | $0–$100k |

| Student loans | $100k–$250k |

| Supporting parents | $250k+ |

Married, No Kids

| Situation | Coverage |

|---|---|

| One income | $400k–$700k |

| Two incomes | $300k–$500k |

Family with Children

| Family Type | Typical Range |

|---|---|

| 1 Child | $500k–$800k |

| 2–3 Kids | $700k–$1M |

| 4+ Kids | $1M+ |

Self-Employed / Business Owner

Needs more protection:

✔ Business loans

✔ Partner buyouts

✔ Income instability

Often: $750k–$1.5M+

How Age Affects Coverage Needs

| Age Group | Focus |

|---|---|

| 20s | Lock low rates |

| 30s | Family protection |

| 40s | Mortgage + college |

| 50s | Reduce gradually |

| 60+ | Estate planning |

Buy earlier = cheaper forever.

Real-Life Case Study (USA)

Michelle — HR Manager, Colorado

Age: 36

Income: $72,000

Kids: 2

Mortgage: $240,000

Old policy: $250,000 ❌

Recalculation:

Debts: $18,000

Income (10 yrs): $720,000

Mortgage: $240,000

Education: $120,000

Total: $1,098,000

New policy: $1M

Cost: $42/month

Now fully protected.

How Term Length Matches Coverage Amount

Your term should cover your highest-risk years.

| Life Stage | Best Term |

|---|---|

| Young kids | 25–30 yrs |

| Teens | 15–20 yrs |

| Empty nest | 10 yrs |

Example:

Age 35 + 25-year term = protection till 60.

How Much Does This Coverage Cost?

Healthy Non-Smoker Example (20-Year Term)

| Age | $500k | $1M |

|---|---|---|

| 30 | $22 | $38 |

| 40 | $45 | $80 |

| 50 | $95 | $170 |

Double coverage ≠ double stress.

It’s often affordable.

Employer Insurance: Why It’s Not Enough

| Feature | Employer Plan | Personal Term |

|---|---|---|

| Average Cover | $50k–$100k | $500k+ |

| Portability | No | Yes |

| Control | Employer | You |

Employer insurance is a bonus, not a solution.

Adjusting for Savings & Investments

If you already have:

✔ Retirement savings

✔ Emergency fund

✔ Investments

You may reduce coverage slightly.

Example:

Need: $800k

Savings: $200k

New cover: $600k

But don’t cut too much.

Smart 6-Step Coverage Calculator

Follow this:

1️⃣ List all debts

2️⃣ Multiply income × 10

3️⃣ Add mortgage

4️⃣ Add education fund

5️⃣ Subtract savings

6️⃣ Round up

This gives safe coverage.

Internal Links (MoneySense America)

👉 “What Is Term Life Insurance in US Explained”

moneysenseamerica.blogspot.com👉 “Emergency Fund Planning for US Families”

moneysenseamerica.blogspot.com👉 “Best Health Insurance for Self-Employed in US”

moneysenseamerica.blogspot.com

Helpful Videos & Learning Resources

Recommended Learning

How Much Life Insurance Do You Need

https://www.youtube.com/watch?v=4GZx3ZKzZ9ITerm Life Insurance Explained

https://www.youtube.com/watch?v=Y3u0Z6yF0KkDIME Method Guide

https://www.youtube.com/watch?v=5v5s8kT4mA0Family Financial Planning Basics

https://www.youtube.com/watch?v=H5Zp3Z0m6jE

(Search official finance channels for updates.)

Frequently Asked Questions (FAQ)

Q1: Is $100,000 life insurance enough?

Usually no for families. Most need $300k–$1M+.

Q2: Can I buy multiple policies?

Yes. Many people combine policies.

Q3: Should both spouses be insured?

Yes, especially if both contribute to family life.

Q4: Does stay-at-home parent need insurance?

Yes. Childcare replacement is expensive.

Q5: Can I reduce coverage later?

Yes. You can adjust as debts decrease.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute financial, legal, or insurance advice. Life insurance needs, pricing, and eligibility vary by individual, state, and insurer. Always consult licensed insurance professionals and official regulatory resources before purchasing coverage. MoneySense America and the author are not responsible for decisions made based on this content.

Bibliography & References

National Association of Insurance Commissioners (NAIC)

https://www.naic.orgInternal Revenue Service — Life Insurance Rules

https://www.irs.govConsumer Financial Protection Bureau — Financial Protection

https://www.consumerfinance.govInvestopedia — Life Insurance Coverage Guide

https://www.investopedia.comU.S. Bureau of Labor Statistics — Income Data

https://www.bls.gov

Final Takeaway: Protect What Matters Most

Remember this simple rule:

💡 Life insurance should replace your life’s financial value.

Not too little.

Not wasteful.

Just right.

If your family can live securely without debt, stress, or sacrifice — you chose correctly.

Buy early.

Review every 3–5 years.

Adjust as life changes.

With the right coverage, your love becomes lifelong security.

Comments

Post a Comment