401(k) Explained Simply: The Complete Beginner Guide for American Investors (2026)

401(k) Explained Simply: The Complete Beginner Guide for American Investors (2026)

Learn how a 401(k) works, employer matching, tax advantages, contribution limits, and smart retirement strategies for beginner American investors.

401(k) Explained Simply for Beginner American Investors

If you work in the United States, there is a very high chance you have heard about the 401(k) retirement plan.

But many beginners still feel confused.

Questions like these are common:

What exactly is a 401(k)?

How does it help with retirement?

What does employer matching mean?

How much should I contribute?

The truth is simple: a 401(k) is one of the most powerful wealth-building tools available to American workers.

In this guide, we will explain everything in a simple, practical way so beginner investors can understand how a 401(k) works.

What Is a 401(k)?

A 401(k) is a retirement savings plan offered by many employers in the United States.

It allows employees to save and invest part of their paycheck before taxes are deducted.

The plan was created under section 401(k) of the U.S. tax code, which is how it got its name.

When you contribute money to a 401(k):

The money is automatically taken from your paycheck

It goes into a retirement investment account

It grows over time through investments

The plan is regulated by the Internal Revenue Service and follows specific tax rules.

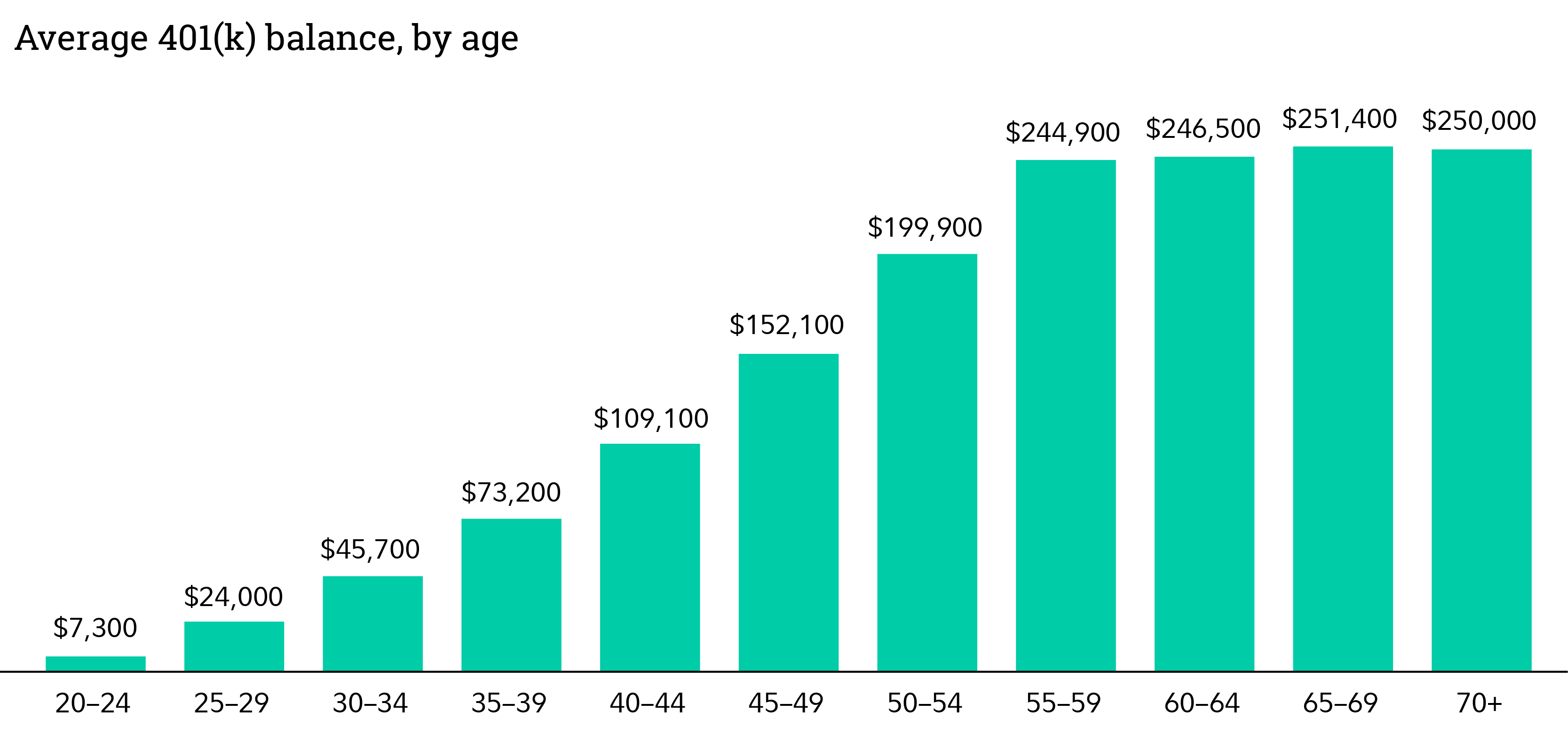

How a 401(k) Works

401k retirement savings concept USA

Employee reviewing 401k retirement statement

401k growth chart illustration

Financial advisor explaining workplace retirement plan

Here is a simple step-by-step explanation.

You choose a percentage of your salary to contribute.

The money is automatically deducted from your paycheck.

It goes into your 401(k) account.

The money is invested in funds such as stocks, bonds, or mutual funds.

The investments grow over time.

You usually cannot withdraw the money until age 59½ without penalties.

Why the 401(k) Is Powerful

The 401(k) plan has three major advantages:

1. Tax Benefits

Traditional 401(k) contributions reduce your taxable income.

Example:

Salary = $60,000

401(k) contribution = $6,000

Taxable income becomes $54,000.

This means you pay less income tax today.

2. Employer Matching

Many companies match employee contributions.

Example:

Employer match policy:

50% match up to 6% of salary

Salary = $60,000

Employee contributes 6% = $3,600

Employer contributes = $1,800

That is free money added to your retirement account.

3. Compound Growth

Over decades, investment growth compounds.

Even small monthly contributions can become large retirement savings.

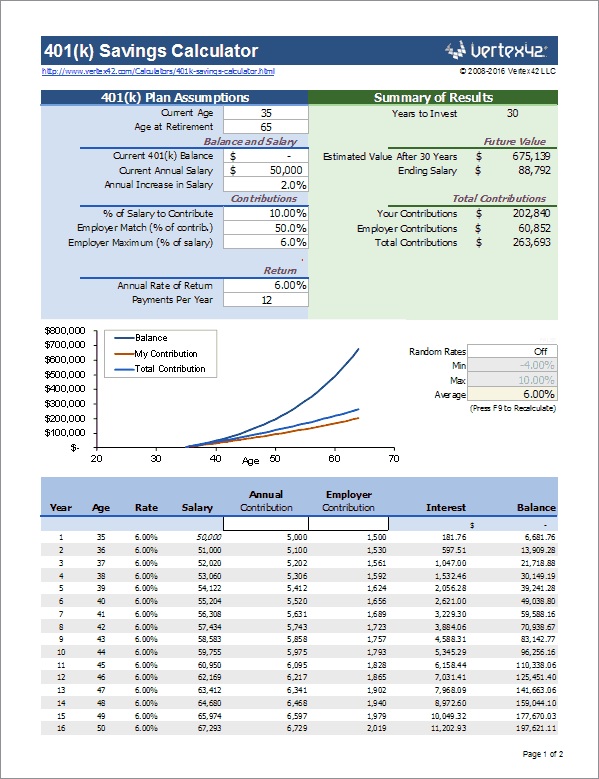

Chart: Long-Term 401(k) Growth Example

Monthly Contribution: $400

Employer Match: $200

Average Annual Return: 7%

Investment Period: 30 Years

Estimated Portfolio Value: $730,000+

This example shows how powerful consistent investing can be.

Types of 401(k) Plans

There are two main types.

Traditional 401(k)

Contributions are made before taxes.

Taxes are paid when you withdraw money in retirement.

Roth 401(k)

Contributions are made after taxes.

Withdrawals during retirement are tax-free.

Understanding this difference is important. You can learn more in our article

“Roth IRA vs Traditional IRA Explained for Beginner Investors” (Internal Link).

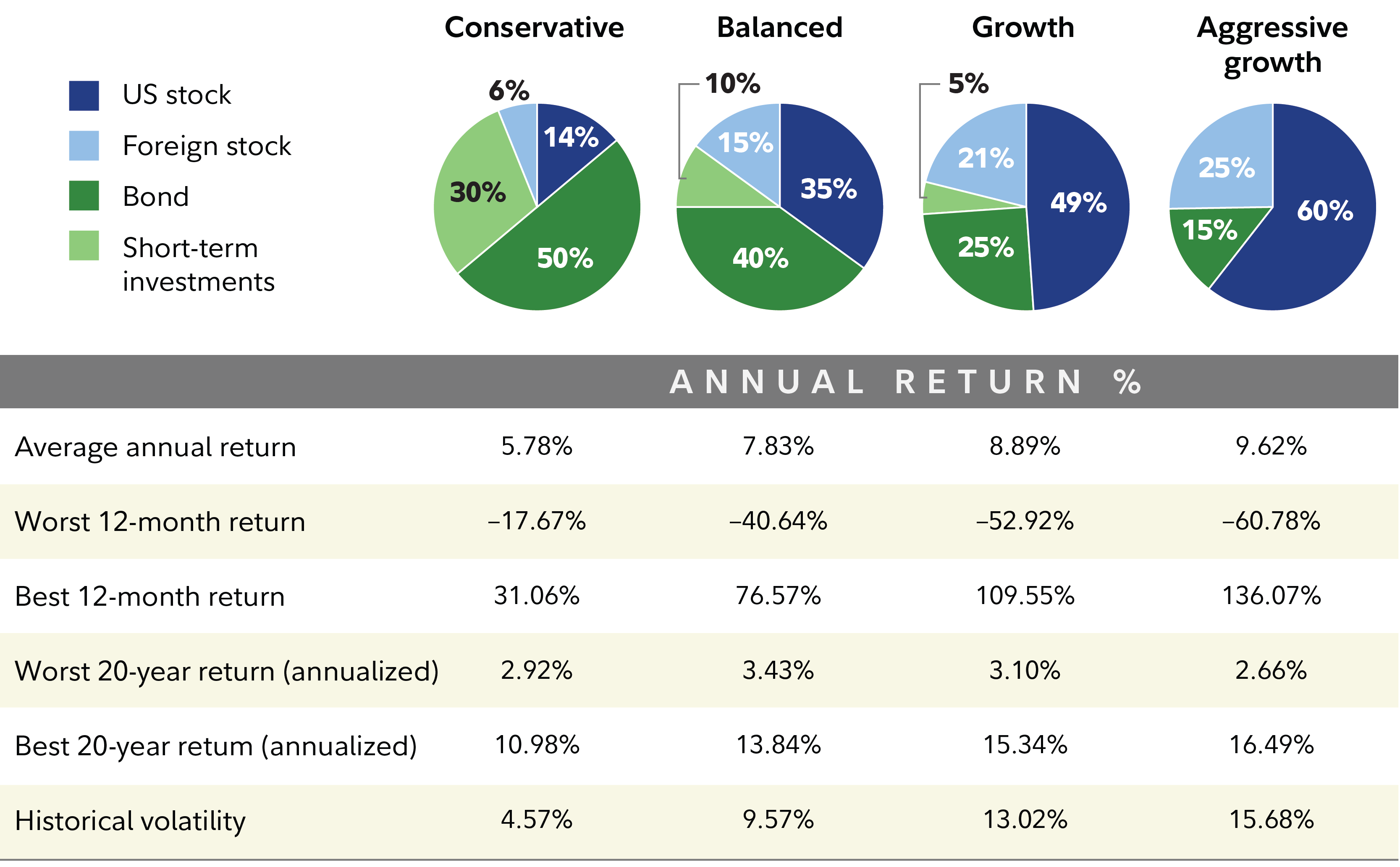

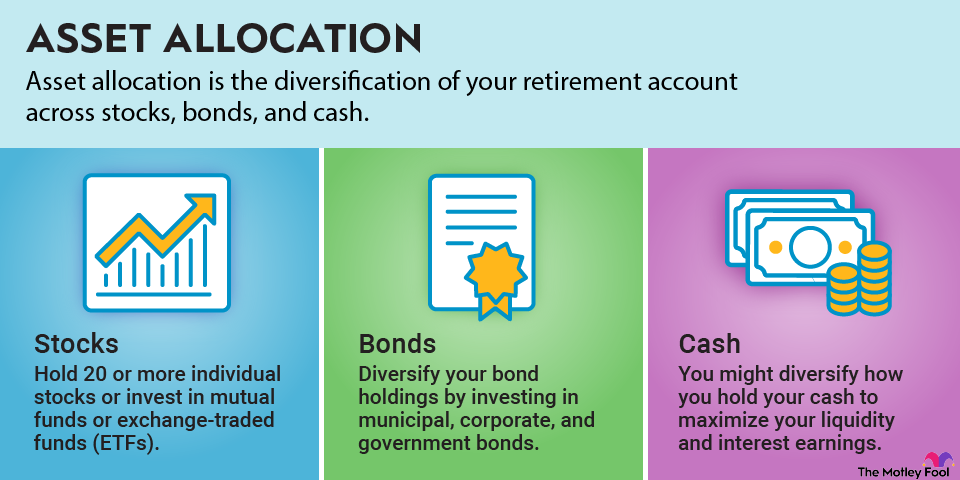

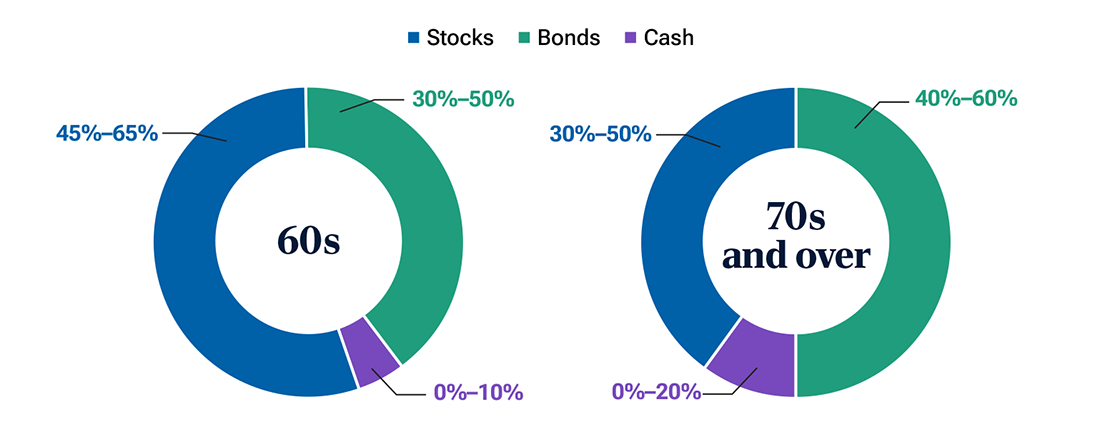

Investment Options Inside a 401(k)

Diversified retirement portfolio allocation

Target date retirement fund concept

Stock bond asset allocation chart

Index fund retirement strategy USA

Your 401(k) usually offers a list of investment options such as:

Index funds

Bond funds

Target-date retirement funds

Many plans include funds tracking the S&P 500.

If you want to understand mutual funds better, read our article

“Mutual Funds for Beginner American Investors Explained” (Internal Link).

Contribution Limits

Contribution limits are set by the Internal Revenue Service.

Typical limits (example):

| Age | Annual Contribution Limit |

|---|---|

| Under 50 | $23,000 |

| 50 and older | $30,500 (includes catch-up contribution) |

Employer contributions are separate and increase total savings.

Example of a Beginner 401(k) Strategy

Let’s look at a realistic example.

Emily works in California and earns $65,000 per year.

Her employer offers:

100% match on first 4%

Emily contributes 4% of salary = $2,600

Employer also contributes $2,600

Total annual contribution = $5,200

If invested consistently for 30 years, this could grow into hundreds of thousands of dollars.

Simple Retirement Saving Flow

Build Emergency Savings

↓

Pay High Interest Debt

↓

Contribute to 401(k) (Get Employer Match)

↓

Open Roth IRA

↓

Invest in ETFs or Mutual Funds

↓

Increase Contributions Over Time

If you are just starting your investing journey, read our guide

“What Is Investing for Beginner Americans” (Internal Link).

Common Beginner Mistakes

Many Americans make simple mistakes with their 401(k).

Not contributing enough to get employer match

This is essentially turning down free money.

Choosing overly conservative investments

Young investors often choose low-growth funds that limit long-term gains.

Cashing out early

Early withdrawals before age 59½ may result in:

Income tax

10% penalty

Ignoring fees

High management fees can reduce long-term returns.

When Can You Withdraw From a 401(k)?

Generally, withdrawals are allowed after age 59½.

Early withdrawals may trigger:

Income tax

10% penalty

Some exceptions exist for:

Hardship withdrawals

Disability

First-time home purchase (depending on plan rules)

Educational Resources

Investor education resources include:

U.S. Securities and Exchange Commission

https://www.investor.govFinancial Industry Regulatory Authority

https://www.finra.org

Market information from

New York Stock Exchange

https://www.nyse.com

Reference Video

401(k) Basics Explained

https://www.youtube.com/watch?v=example-401k-guide

FAQ

What is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows workers to invest part of their salary for retirement.

Is employer matching guaranteed?

No. Matching policies vary by company, but many employers offer partial matches.

Can I have both a 401(k) and an IRA?

Yes. Many Americans contribute to both for better retirement diversification.

Can I change investments inside my 401(k)?

Yes. Most plans allow you to adjust investment allocations.

What happens to my 401(k) if I change jobs?

You can usually:

Roll it into a new employer plan

Transfer it to an IRA

Leave it with the previous employer (depending on balance)

Statutory Disclaimer

This article is for informational and educational purposes only and does not constitute financial, tax, or investment advice. Investment decisions involve risk, including possible loss of principal. Tax laws and retirement rules may change over time. Readers should consult a licensed financial advisor or tax professional before making financial decisions. moneysenseamerica.blogspot.com and the author are not responsible for financial actions taken based on this information.

Bibliography

Internal Revenue Service Retirement Plan Resources

U.S. Securities and Exchange Commission Investor Education

FINRA Investor Education Foundation

Federal Reserve Personal Finance Resources

Investment Company Institute Research

Final Thoughts

A 401(k) is not just a retirement account — it is a powerful wealth-building system available to millions of American workers.

By combining:

tax advantages

employer contributions

long-term investing

it allows ordinary workers to build significant retirement savings.

The most important step is simple: start early and contribute consistently.

For more practical financial guidance, explore other beginner guides on moneysenseamerica.blogspot.com, including:

What Is Investing for Beginner Americans

Stocks vs Bonds for Beginner Investors

What Is ETF and How It Works

Roth IRA vs Traditional IRA Explained

Small steps today can lead to financial freedom tomorrow.

Comments

Post a Comment