Obamacare Explained Simply: ACA Plans, Costs, Subsidies & How It Works in the US

Obamacare in the US Explained Simply — Plans, Costs & How It Really Works (2026 Guide)

Obamacare Explained Simply: ACA Plans, Costs, Subsidies & How It Works in the US

Learn how Obamacare (Affordable Care Act) works in the US. Understand ACA plans, premiums, subsidies, Medicaid expansion, enrollment rules, and real-life examples.

“Family enrolling in Obamacare health insurance on HealthCare.gov”

“Couple reviewing ACA health insurance plan documents at home”

“Young adult comparing Affordable Care Act insurance plans online”

“Patient paying copay under ACA health insurance plan”

Many Americans hear the word “Obamacare” and feel confused.

Some think it’s free healthcare.

Some think it’s expensive.

Some don’t know if it applies to them.

The truth is simpler:

Obamacare is the Affordable Care Act (ACA) — a law that helps Americans get health insurance, especially if they don’t have it through a job.

In this guide, we’ll explain how Obamacare works in simple, practical language — with real examples and clear charts.

What Is Obamacare?

“Obamacare” is the popular name for the Affordable Care Act (ACA).

It was signed into law in 2010 and is regulated by:

Centers for Medicare & Medicaid Services

Its main goal:

✔ Make health insurance available

✔ Protect people with pre-existing conditions

✔ Offer income-based subsidies

✔ Expand Medicaid

Who Can Use Obamacare?

Obamacare helps people who:

✔ Don’t have employer insurance

✔ Are self-employed

✔ Work part-time

✔ Lost their job

✔ Retired early (before Medicare)

If you already have good employer insurance, you may not need it.

How Obamacare Works (Step-by-Step)

Step 1: Visit HealthCare.gov

This is the official marketplace website where you compare plans.

You enter:

Age

Income

Family size

Zip code

The system calculates your subsidy.

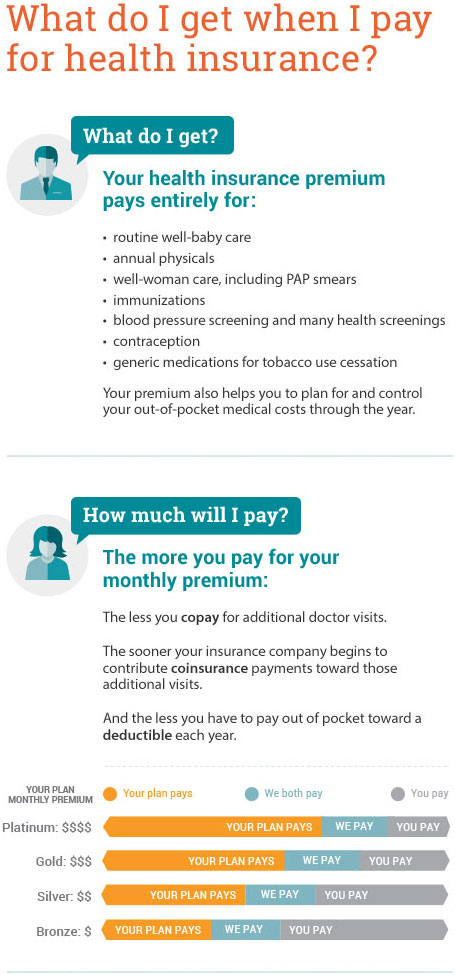

Step 2: See Plan Options (Metal Levels)

ACA plans come in 4 levels:

| Plan | Monthly Premium | Out-of-Pocket Cost | Best For |

|---|---|---|---|

| Bronze | Lowest | Highest | Healthy people |

| Silver | Moderate | Moderate | Most families |

| Gold | Higher | Lower | Frequent doctor visits |

| Platinum | Highest | Lowest | Chronic conditions |

Step 3: Apply Subsidy

Your income decides how much help you receive.

Subsidies reduce monthly premiums.

Real Example: Single Adult in Texas

Age: 30

Income: $35,000

Silver Plan:

Without subsidy → $420/month

With subsidy → $115/month

Annual savings: $3,660

That’s how Obamacare makes insurance affordable.

Key Obamacare Benefits

1️⃣ No Denial for Pre-Existing Conditions

Before ACA, insurers could reject you for:

Diabetes

Cancer

Asthma

Pregnancy

Now they cannot.

2️⃣ Subsidies Based on Income

Lower income = higher subsidy.

Example:

| Income | Monthly Premium (Silver Plan) |

|---|---|

| $28,000 | $75 |

| $40,000 | $150 |

| $55,000 | $260 |

Subsidies are managed through tax credits regulated by the

Internal Revenue Service.

3️⃣ Medicaid Expansion

Many states expanded Medicaid under Obamacare.

If your income is low, you may qualify for:

✔ $0 premium

✔ Low copays

✔ Full coverage

Check your state eligibility.

4️⃣ Essential Health Benefits

All ACA plans must cover:

✔ Emergency services

✔ Hospital care

✔ Maternity care

✔ Prescription drugs

✔ Mental health services

✔ Preventive care

This prevents “junk insurance.”

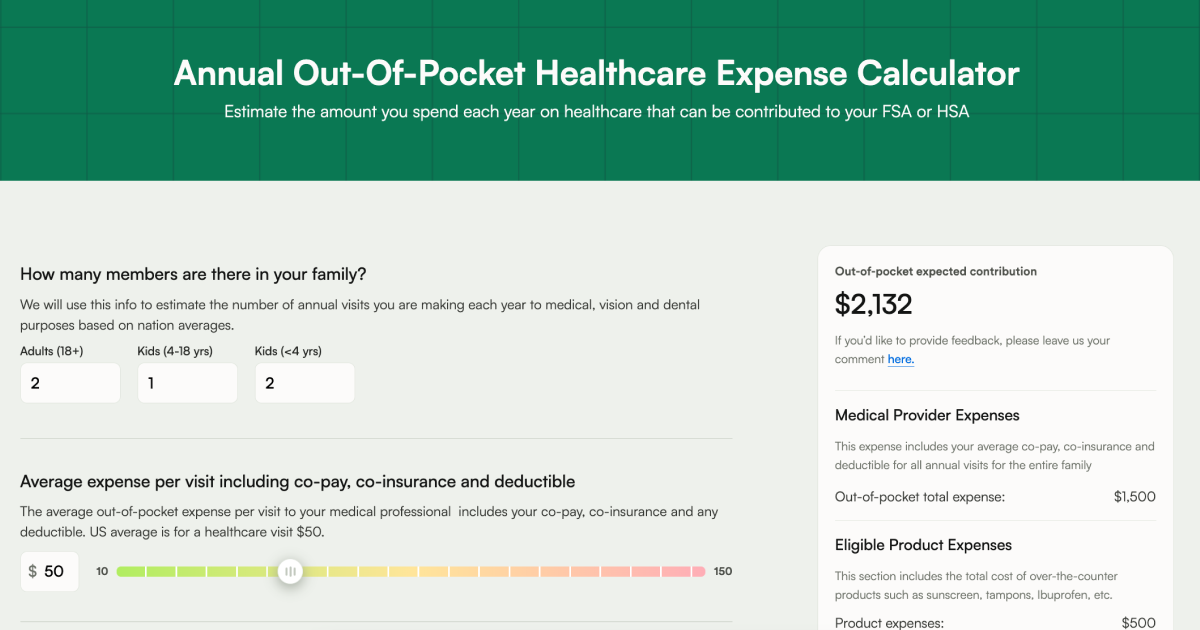

How Much Does Obamacare Cost?

It depends on:

Income

State

Age

Plan level

Cost Example Chart

Family of 3 — Florida

| Plan | Monthly Premium (With Subsidy) |

|---|---|

| Bronze | $140 |

| Silver | $210 |

| Gold | $330 |

Bronze is cheapest monthly.

Gold is cheapest if you need frequent care.

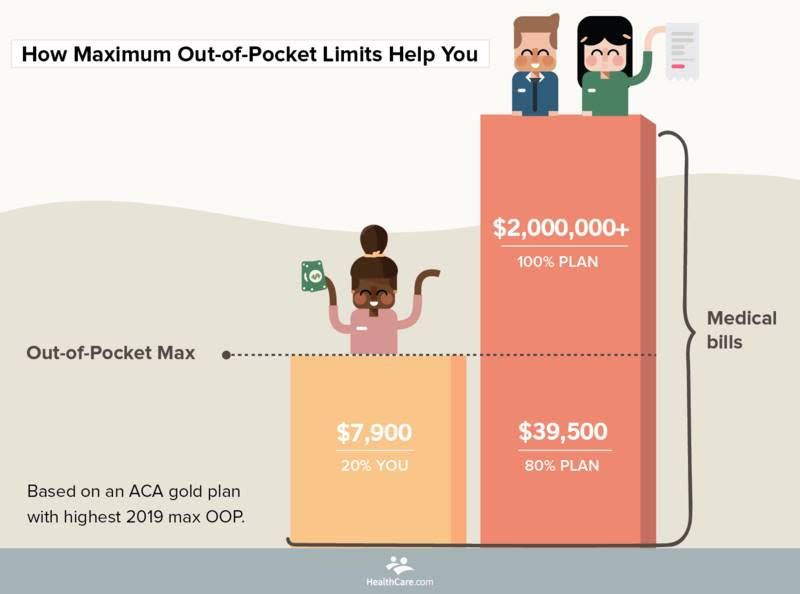

Important Health Insurance Terms Explained

| Term | Meaning |

|---|---|

| Premium | Monthly payment |

| Deductible | Amount you pay first |

| Copay | Flat visit fee |

| Coinsurance | % of cost |

| Out-of-Pocket Max | Maximum yearly spending |

Example:

Hospital bill: $10,000

Deductible: $2,000

Coinsurance: 20%

You pay:

$2,000 + $1,600 = $3,600

Insurance pays the rest.

Who Should Choose Bronze vs Silver vs Gold?

Choose Bronze If:

✔ You are healthy

✔ Rarely visit doctor

✔ Want lowest premium

Choose Silver If:

✔ You qualify for cost-sharing reductions

✔ Moderate healthcare use

Choose Gold If:

✔ Chronic illness

✔ Regular prescriptions

✔ Ongoing treatment

Common Obamacare Mistakes

❌ Missing Open Enrollment

❌ Underestimating income

❌ Choosing cheapest premium blindly

❌ Not checking doctor network

❌ Ignoring subsidy updates

These errors can cost thousands.

Open Enrollment Period

You can enroll:

✔ During Open Enrollment (usually Nov–Jan)

✔ Or after special life events (job loss, marriage, baby)

Outside this window, enrollment is limited.

Helpful Videos & Learning Resources

Obamacare Explained Simply

https://www.youtube.com/watch?v=Y3u0Z6yF0KkHow ACA Subsidies Work

https://www.youtube.com/watch?v=4GZx3ZKzZ9IBronze vs Silver vs Gold Plans

https://www.youtube.com/watch?v=5v5s8kT4mA0Health Insurance Basics

https://www.youtube.com/watch?v=H5Zp3Z0m6jE

(Search official government sources for updates.)

Internal Links (MoneySense America)

👉 “How Health Insurance Works in the US”

moneysenseamerica.blogspot.com👉 “Cheapest Health Insurance Plans in US”

moneysenseamerica.blogspot.com👉 “Best Health Insurance for Self-Employed in US”

moneysenseamerica.blogspot.com

Frequently Asked Questions (FAQ)

Q1: Is Obamacare free?

No. But subsidies can reduce premiums significantly.

Q2: Can I be denied coverage?

No, not for pre-existing conditions.

Q3: Is Obamacare only for unemployed people?

No. Many working Americans use it.

Q4: What happens if my income changes?

Update your marketplace account immediately.

Q5: Do ACA plans cover emergencies?

Yes. Emergency services are required.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute legal, medical, or financial advice. Health insurance rules, subsidies, and eligibility requirements vary by state and may change. Always verify details through official government websites or licensed insurance professionals. MoneySense America and the author are not responsible for actions taken based on this information.

Bibliography & References

U.S. Department of Health and Human Services

https://www.hhs.govCenters for Medicare & Medicaid Services

https://www.cms.govHealthCare.gov — Official Marketplace

https://www.healthcare.govKaiser Family Foundation — ACA Data

https://www.kff.orgInternal Revenue Service — Premium Tax Credits

https://www.irs.gov

Final Takeaway: Obamacare Made Insurance More Accessible

Remember this:

🏥 Obamacare is not perfect — but it protects millions of Americans from financial disaster.

It ensures:

✔ No denial for pre-existing conditions

✔ Income-based help

✔ Essential coverage standards

When used wisely, ACA plans make healthcare more affordable and predictable.

Comments

Post a Comment