How to Reduce Student Loan Payments in the USA: Legal Ways to Lower Your EMI & Save Money

How to Reduce Student Loan Payments in the USA: A Practical Guide for Working Adults (2026 Edition)

How to Reduce Student Loan Payments in the USA: Legal Ways to Lower Your EMI & Save Money

Learn proven ways to reduce student loan payments in the USA. Discover income-driven plans, refinancing, forgiveness, deferment, and real-life strategies for working adults.

For millions of Americans, student loans feel like a second rent payment.

Every month, hundreds of dollars go to lenders before savings, travel, or family goals. Many working adults ask:

“Is there any legal way to reduce my student loan payment?”

The answer is: Yes — in many ways.

If you understand the system, you can lower your monthly bill, reduce stress, and protect your future.

This guide explains simple, legal, and practical methods to reduce student loan payments in the USA.

Understanding Who Controls Your Student Loans

Most federal student loans are managed by the

U.S. Department of Education

through its student aid system.

Information and tools are provided by

Federal Student Aid

at https://studentaid.gov.

Private loans are handled by banks and lenders.

👉 Your options depend on whether your loan is federal or private.

Step 1: Know Your Loan Type (Very Important)

Before changing anything, confirm:

✔ Federal loans

✔ Private loans

✔ Mixed loans

Check at: studentaid.gov

Why This Matters

| Loan Type | Payment Reduction Options |

|---|---|

| Federal | Many (IDR, forgiveness, pause) |

| Private | Few (refinance, hardship) |

(Source: Consumer Financial Protection Bureau)

Most powerful tools apply to federal loans.

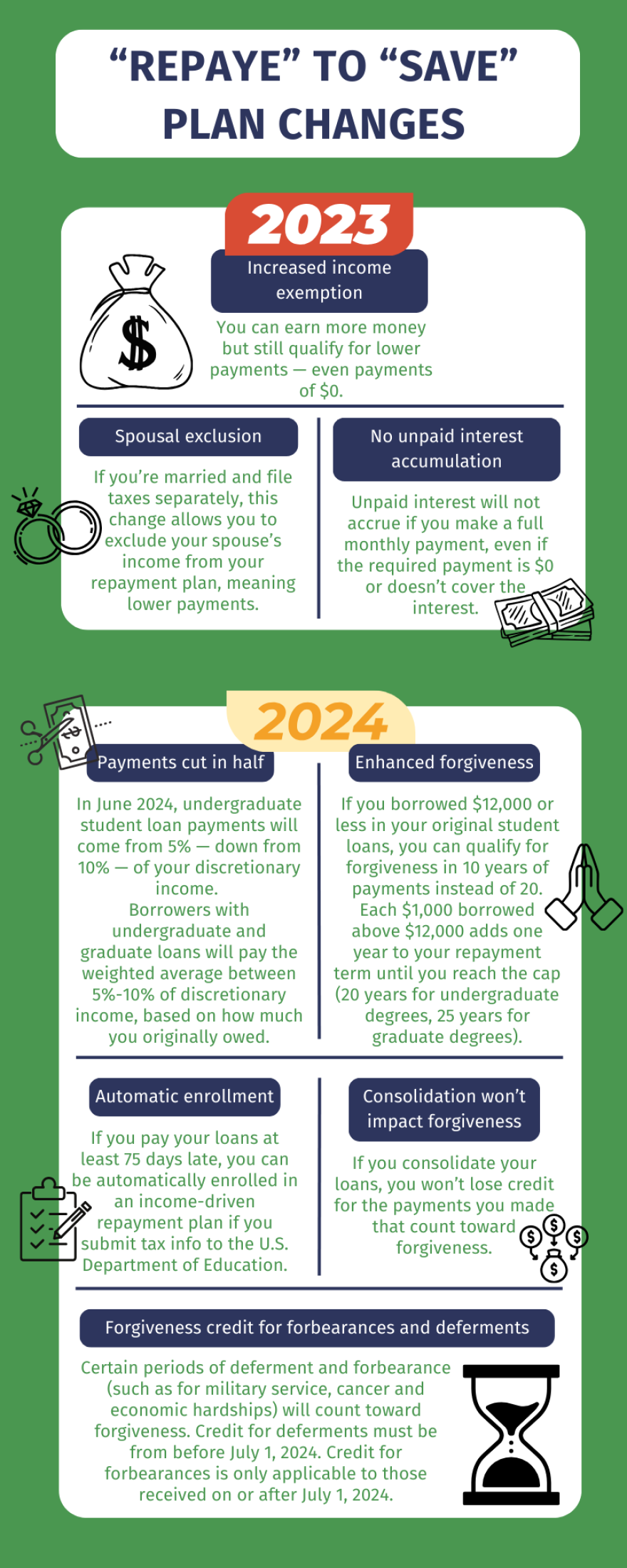

Step 2: Use Income-Driven Repayment Plans (Best Tool)

Income-Driven Repayment (IDR) plans link your payment to your salary.

Main IDR Plans

| Plan | Payment | Best For |

|---|---|---|

| SAVE | ~5% income | Most borrowers |

| PAYE | ~10% income | Moderate income |

| IBR | ~10–15% | Older loans |

(Source: Investopedia)

Example: How IDR Reduces Payments

Kevin — Warehouse Supervisor (Ohio)

Loan: $38,000

Income: $42,000

Standard payment: $420

SAVE plan payment: $145

👉 Monthly savings: $275

That’s $3,300 per year.

Who Should Use IDR?

✔ Low or moderate income

✔ Family dependents

✔ Unstable job

✔ Public sector workers

Apply at studentaid.gov.

Step 3: Apply for Public Service Loan Forgiveness (PSLF)

If you work in:

✔ Government

✔ Public schools

✔ Nonprofits

✔ Public hospitals

You may qualify for Public Service Loan Forgiveness.

How It Works

Make 120 qualifying payments (10 years)

Use IDR plan

Balance forgiven

Example:

$45,000 remaining → $0

Private loans ❌ Not eligible.

Step 4: Use Deferment and Forbearance (Short-Term Relief)

If you face hardship:

Job loss

Medical emergency

Family crisis

You can pause payments.

Options

| Option | Interest | Use |

|---|---|---|

| Deferment | Sometimes paid | Temporary break |

| Forbearance | Continues | Last option |

Use only for emergencies — interest grows.

Step 5: Refinance Carefully (For Some Borrowers)

Refinancing means replacing old loans with a new private loan.

When It Helps

✔ Strong credit (700+)

✔ Stable job

✔ High interest rate now

Example

Old rate: 8%

New rate: 5%

Savings: $4,000+

⚠ Warning: You lose federal protections forever.

Step 6: Ask for Employer Student Loan Help

Many U.S. employers now offer loan benefits.

Examples:

Amazon

Google

Hospitals

Government agencies

They may pay:

$50–$200/month toward loans.

Always ask HR.

Step 7: Lower Payments with Strategic Consolidation

Federal Direct Consolidation:

Combines loans

Simplifies payments

Keeps federal benefits

It may:

✔ Extend term

✔ Lower EMI

❌ Increase total interest

Use when cash flow matters.

Step 8: Reduce Payments with Smart Budgeting

Small changes help.

Monthly Saving Ideas

| Change | Savings |

|---|---|

| Cancel subscriptions | $60 |

| Cook more | $120 |

| Cheaper phone plan | $50 |

| Insurance review | $40 |

Extra $270 → covers IDR payment.

Step 9: Use Tax Benefits

The U.S. tax system helps borrowers.

You may deduct up to $2,500 of student loan interest.

Check rules via

Internal Revenue Service.

This reduces real cost.

Step 10: Combine Multiple Methods (Best Strategy)

Smart borrowers mix tools.

Ideal Combination

✔ IDR plan

✔ Employer help

✔ Budget savings

✔ Occasional extra payments

This keeps payment low and debt shrinking.

Payment Reduction Comparison Chart

Example: $35,000 Federal Loan

| Method | Monthly Payment |

|---|---|

| Standard | $380 |

| IDR (SAVE) | $140 |

| Extended | $210 |

| Refinance | $260 |

| PSLF (IDR) | $140 → $0 later |

Best option: Depends on job and income.

Real-Life Case Study (USA)

Angela — Social Worker (Michigan)

Loan: $48,000

Income: $46,000

Family: 2 kids

Strategy:

✔ SAVE plan

✔ PSLF

✔ Employer support

Payment: $155/month

After 10 years: Balance forgiven.

Saved: $30,000+

Common Mistakes That Increase Payments

Avoid these:

❌ Ignoring IDR plans

❌ Missing recertification

❌ Refinancing too early

❌ Defaulting

❌ Skipping employer benefits

These mistakes cost thousands.

Internal Links (MoneySense America)

Connect this post with:

👉 “How Student Loans Work in the USA”

moneysenseamerica.blogspot.com👉 “Federal vs Private Student Loans in the USA”

moneysenseamerica.blogspot.com👉 “Loan Prepayment Pros and Cons in USA”

moneysenseamerica.blogspot.com

Helpful Videos & Learning Resources

Recommended Viewing

SAVE Plan Explained (Federal Student Aid)

https://www.youtube.com/watch?v=0xZ8B1vZK0MIncome-Driven Repayment Guide

https://www.youtube.com/watch?v=K9N5S4WZ9xEPSLF Walkthrough

https://www.youtube.com/watch?v=7cJ4QZpF5qMStudent Loan Budgeting Tips

https://www.youtube.com/watch?v=3LQmRZP2kHg

(Search official channels for updates.)

Frequently Asked Questions (FAQ)

Q1: What is the fastest way to reduce payments?

Switch to the SAVE or IDR plan if eligible.

Q2: Can private loans use IDR?

No. Only federal loans qualify.

Q3: Should I refinance to reduce EMI?

Only if you have stable income and high interest.

Q4: Do missed payments increase future costs?

Yes. They damage credit and add penalties.

Q5: Will forgiveness be taxed?

Sometimes. Check current IRS rules.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute legal, financial, or tax advice. Student loan regulations, interest rates, and government programs change regularly. Consult official government resources, certified financial advisors, or student loan counselors before making repayment decisions. MoneySense America and the author are not responsible for actions taken based on this content.

Bibliography & References

Federal Student Aid — U.S. Department of Education

https://studentaid.govConsumer Financial Protection Bureau — Student Loan Tools

https://www.consumerfinance.govInvestopedia — Student Loan Repayment Guides

https://www.investopedia.comInternal Revenue Service — Student Loan Tax Benefits

https://www.irs.govNational Center for Education Statistics — College Costs

https://nces.ed.gov

Final Takeaway: Your 3 Golden Rules

Remember this:

📌 Use IDR first

📌 Protect federal benefits

📌 Review yearly

Reducing student loan payments is not about shortcuts.

It is about using the system wisely.

With the right plan, your monthly burden can drop — and your future can grow.

Comments

Post a Comment