How to Lower Medical Bills Legally in the US: Proven Ways to Reduce Hospital Costs

How to Lower Medical Bills Legally in the US — A Simple, Step-by-Step Guide (2026)

How to Lower Medical Bills Legally in the US: Proven Ways to Reduce Hospital Costs

Learn how to lower medical bills legally in the US. Discover negotiation tips, charity care, insurance appeals, itemized bills, and real examples to save thousands.

“American family reviewing high hospital bill at home”

“Patient negotiating medical bill with hospital billing office”

“Itemized hospital bill being checked online in the USA”

“Couple planning medical payment options with calculator”

“Explanation of Benefits and hospital invoice comparison”

Medical bills in the United States can feel shocking.

Even with insurance, many people open an envelope and think:

“Why is this so high? Did I really use this much care?”

The truth is:

👉 Most Americans overpay medical bills at least once.

👉 Many bills can be reduced — legally and ethically.

Hospitals and insurance systems are complex. Errors, overcharges, and hidden discounts are common.

This guide explains how to lower medical bills legally in the US, in clear and practical language, with real examples.

Who Regulates Medical Billing in the US?

Medical billing and insurance rules are overseen by:

U.S. Department of Health and Human Services

Centers for Medicare & Medicaid Services

Consumer protection is supported by the

Consumer Financial Protection Bureau

Tax-related medical deductions are handled by the

Internal Revenue Service

These agencies make sure hospitals follow federal rules.

Why Medical Bills Are So High in America

Before reducing bills, you should know why they are expensive.

Main reasons:

✔ High hospital operating costs

✔ Complex insurance pricing

✔ Marked-up “list prices”

✔ Administrative fees

✔ Billing errors

Hospitals often charge full retail prices first. Discounts come later — only if you ask.

Step 1: Never Pay a Medical Bill Immediately

This is the biggest mistake Americans make.

Many people think:

“If I don’t pay fast, I’ll get in trouble.”

But most hospitals give 90–180 days before collections.

What To Do First

✔ Read every page

✔ Compare with insurance EOB

✔ Check service dates

✔ Look for duplicates

Take time. Rushing costs money.

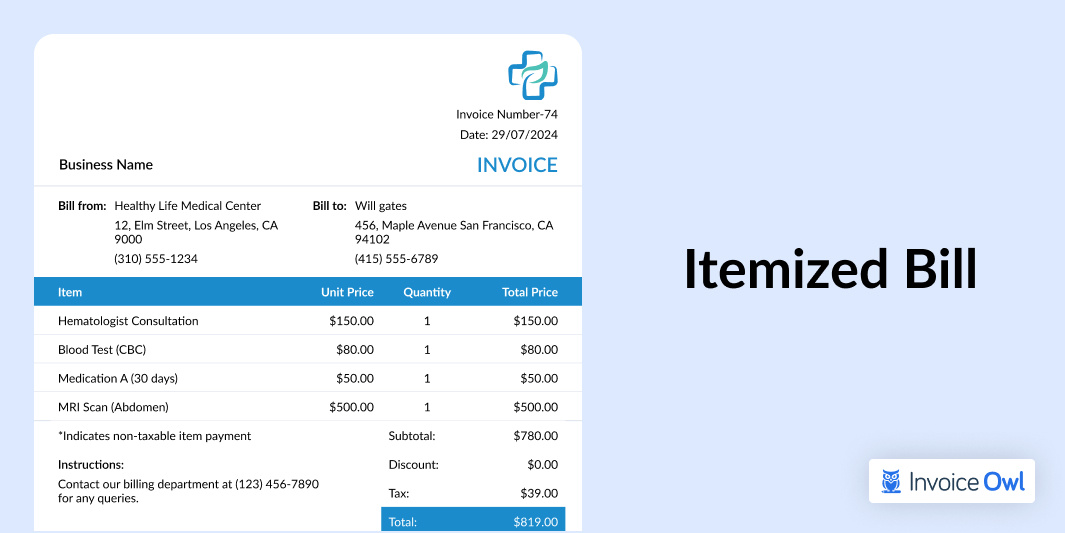

Step 2: Ask for an Itemized Bill (Powerful Tool)

Many hospitals send only summary bills.

You must request:

👉 “Please send me a full itemized bill.”

Why This Works

Itemized bills reveal:

✔ Duplicate charges

✔ Wrong procedures

✔ Extra supplies

✔ Overpriced tests

Studies show up to 80% of medical bills contain errors.

Example: Karen — Missouri

Original bill: $6,800

After itemized review: Found duplicate lab charge

New bill: $5,200

Saved: $1,600

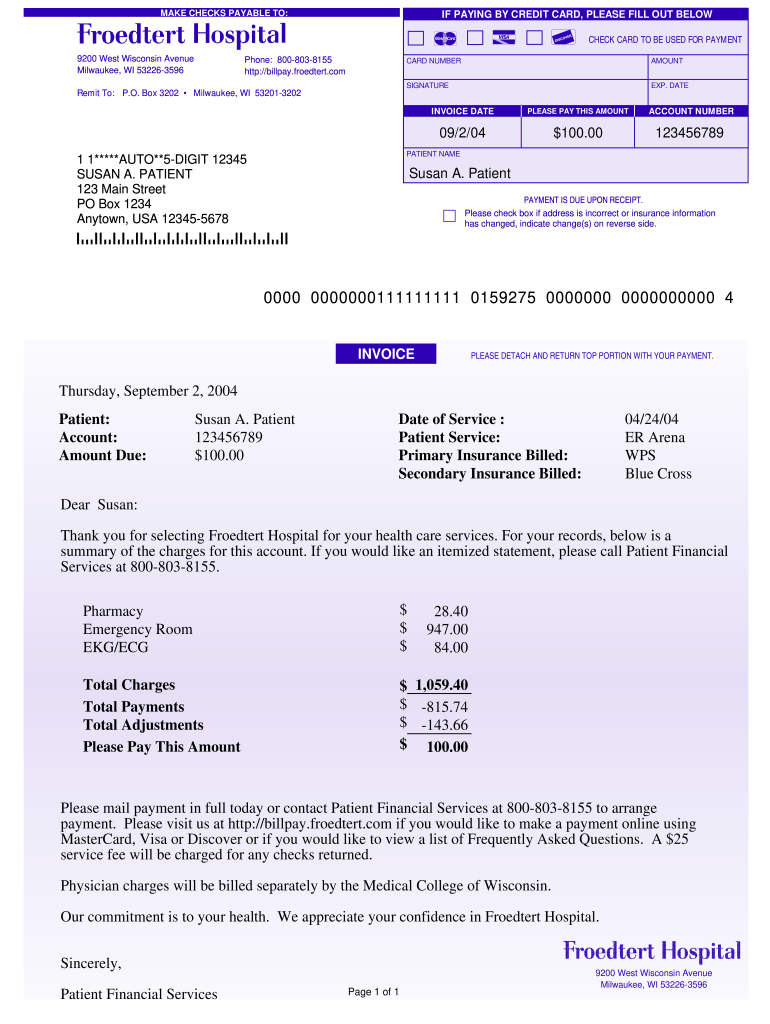

Step 3: Compare Bill with Your EOB

Your insurance sends an Explanation of Benefits (EOB).

This is not a bill.

It shows:

| Item | Meaning |

|---|---|

| Charged | What hospital asked |

| Allowed | What insurer approved |

| Paid | What insurer paid |

| Owe | Your responsibility |

Always compare EOB with hospital bill.

If numbers don’t match → dispute.

Step 4: Check for Billing Errors

Common errors include:

❌ Services you never received

❌ Wrong diagnosis codes

❌ Out-of-network mistakes

❌ Double billing

❌ Upcoding (charging higher service)

What to Say

Call billing office:

“I see a charge for X on March 12. I never received this service. Please review.”

Be calm. Be firm. Take notes.

Step 5: Apply for Hospital Financial Assistance (Charity Care)

Most nonprofit hospitals must offer charity care.

This is required under federal rules.

What Charity Care Can Do

✔ Reduce bill by 20%–100%

✔ Offer free care for low income

✔ Apply even after treatment

Many middle-class families qualify but never apply.

Example: Miguel — Arizona

Income: $48,000

Hospital bill: $9,400

Applied for charity care → 50% discount

New bill: $4,700

Saved: $4,700

Step 6: Negotiate Your Medical Bill

Yes — hospitals negotiate.

And often easily.

When to Negotiate

✔ Large bill

✔ Uninsured

✔ High deductible

✔ Out-of-network care

Simple Script

“I want to pay, but I cannot afford this amount. Can you offer a discount?”

Ask for:

Self-pay discount

Cash discount

Prompt-pay discount

Typical reductions: 20%–60%

Step 7: Set Up an Interest-Free Payment Plan

If you can’t pay at once:

Ask for:

✔ No-interest plan

✔ 12–36 months

✔ Small monthly payments

Example:

$6,000 bill

36 months → $167/month

Much easier.

Step 8: Appeal Insurance Denials

Many claims are wrongly denied.

Do not accept “Denied” immediately.

Appeal Process

Request reason

Submit documents

Ask doctor for letter

File formal appeal

Over 40% of appeals succeed.

Step 9: Use In-Network Providers Always

Out-of-network care causes huge bills.

| Type | Average Cost |

|---|---|

| In-network ER | $1,200 |

| Out-of-network ER | $4,000+ |

Before non-emergency care:

✔ Check provider

✔ Check lab

✔ Check anesthesiologist

One out-of-network doctor can ruin savings.

Step 10: Use Preventive Care (Free Under ACA)

Under ACA rules, many services are free:

✔ Annual checkups

✔ Vaccines

✔ Screenings

✔ Blood pressure tests

Using preventive care avoids future big bills.

Real-Life Case Study (USA)

Robert — Delivery Driver (Florida)

Hospital stay: 2 days

Original bill: $18,500

Steps taken:

✔ Requested itemized bill

✔ Found wrong medication charge

✔ Applied for charity care

✔ Negotiated balance

✔ Set payment plan

Final bill: $6,900

Saved: $11,600

Medical Bill Reduction Comparison Chart

Example: $10,000 Hospital Bill

| Strategy | New Amount |

|---|---|

| No action | $10,000 |

| Itemized review | $8,200 |

| Charity care | $5,400 |

| Negotiation | $4,800 |

| Combined steps | $3,900 |

Best results come from combining methods.

Smart 7-Step System to Lower Bills

Follow this order:

1️⃣ Review bill

2️⃣ Get itemized version

3️⃣ Match with EOB

4️⃣ Check for errors

5️⃣ Apply for assistance

6️⃣ Negotiate

7️⃣ Set payment plan

Never skip steps.

Common Mistakes That Increase Bills

❌ Paying immediately

❌ Ignoring EOB

❌ Not applying for aid

❌ Using collections agencies

❌ Missing appeal deadlines

These mistakes cost thousands.

Helpful Videos & Official Resources

Recommended Learning

Medical Bill Negotiation Guide

https://www.youtube.com/watch?v=Y3u0Z6yF0KkUnderstanding EOB Statements

https://www.youtube.com/watch?v=H5Zp3Z0m6jEHospital Financial Assistance

https://www.youtube.com/watch?v=5v5s8kT4mA0Insurance Appeals Explained

https://www.youtube.com/watch?v=4GZx3ZKzZ9I

(Search official healthcare channels for updates.)

Internal Links (MoneySense America)

👉 “How Health Insurance Works in the US”

moneysenseamerica.blogspot.com👉 “Health Insurance Deductibles in US Explained”

moneysenseamerica.blogspot.com👉 “Cheapest Health Insurance Plans in US”

moneysenseamerica.blogspot.com

Frequently Asked Questions (FAQ)

Q1: Is it legal to negotiate medical bills?

Yes. Hospitals expect negotiations.

Q2: Can I ask for discount after paying?

Sometimes yes. Request a review.

Q3: Will negotiation hurt my credit?

No, if you communicate and pay on time.

Q4: What if bill goes to collections?

You still can negotiate. Act quickly.

Q5: Are medical bills tax deductible?

Sometimes, if expenses exceed IRS limits.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute legal, medical, or financial advice. Medical billing laws, hospital policies, and insurance rules vary by state and provider and may change. Always verify details with your healthcare provider, insurer, or licensed professional. MoneySense America and the author are not responsible for actions taken based on this information.

Bibliography & References

U.S. Department of Health and Human Services

https://www.hhs.govCenters for Medicare & Medicaid Services

https://www.cms.govConsumer Financial Protection Bureau — Medical Debt

https://www.consumerfinance.govKaiser Family Foundation — Healthcare Costs

https://www.kff.orgInternal Revenue Service — Medical Expense Deductions

https://www.irs.gov

Final Takeaway: You Have More Power Than You Think

Remember this:

💡 Medical bills are negotiable — silence is expensive.

If you ask questions, check details, and apply for help, you can often cut bills in half.

Don’t be afraid.

Be polite.

Be persistent.

With the right steps, medical debt does not have to control your life.

Comments

Post a Comment