How Health Insurance Works in the US: Plans, Costs, Deductibles & Smart Tips Explained

How Health Insurance Works in the US — A Simple, Real-Life Guide for Everyday Americans (2026)

How Health Insurance Works in the US: Plans, Costs, Deductibles & Smart Tips Explained

Learn how health insurance works in the US. Understand premiums, deductibles, copays, ACA plans, employer insurance, Medicare, Medicaid, and real examples to save money.

“American family reviewing health insurance options at home”

“Working adult comparing health insurance plans online in the USA”

“Doctor visit copay payment at US clinic”

“Health insurance budgeting with medical bills and notebook”

“Explanation of Benefits EOB health insurance document USA”

Health insurance in the United States often feels confusing, expensive, and overwhelming.

People hear words like premium, deductible, copay, and out-of-pocket maximum — but don’t always know what they really mean.

Yet, one medical emergency without insurance can cost tens of thousands of dollars.

This guide explains how health insurance works in the US in the simplest, most practical way — using real American examples, charts, and step-by-step logic.

Why Health Insurance Is So Important in the US

Unlike many countries, the US does not provide free universal healthcare.

That means:

Doctor visits

Hospital stays

Surgeries

Prescriptions

…can be extremely expensive without insurance.

Example:

| Medical Service | Typical Cost (Without Insurance) |

|---|---|

| ER visit | $1,200 – $3,000 |

| Broken arm | $2,500 – $7,500 |

| 3-day hospital stay | $30,000+ |

| Childbirth | $10,000 – $20,000 |

Health insurance protects you from these shocks.

Who Regulates Health Insurance in the US?

Health insurance rules are set and monitored by:

Centers for Medicare & Medicaid Services

Consumer guidance is also provided through the Affordable Care Act marketplace at HealthCare.gov.

What Is Health Insurance? (Simple Meaning)

Health insurance is a contract.

You pay a fixed amount every month.

The insurance company helps pay your medical bills.

In return, you must follow plan rules like:

✔ Using in-network doctors

✔ Paying deductibles

✔ Paying copays or coinsurance

The 5 Key Health Insurance Terms You Must Know

1. Premium

The monthly amount you pay just to keep insurance active.

Example: $450/month

2. Deductible

The amount you pay before insurance starts paying.

Example: $2,000 per year

3. Copay

A flat fee per visit.

Example: $30 doctor visit

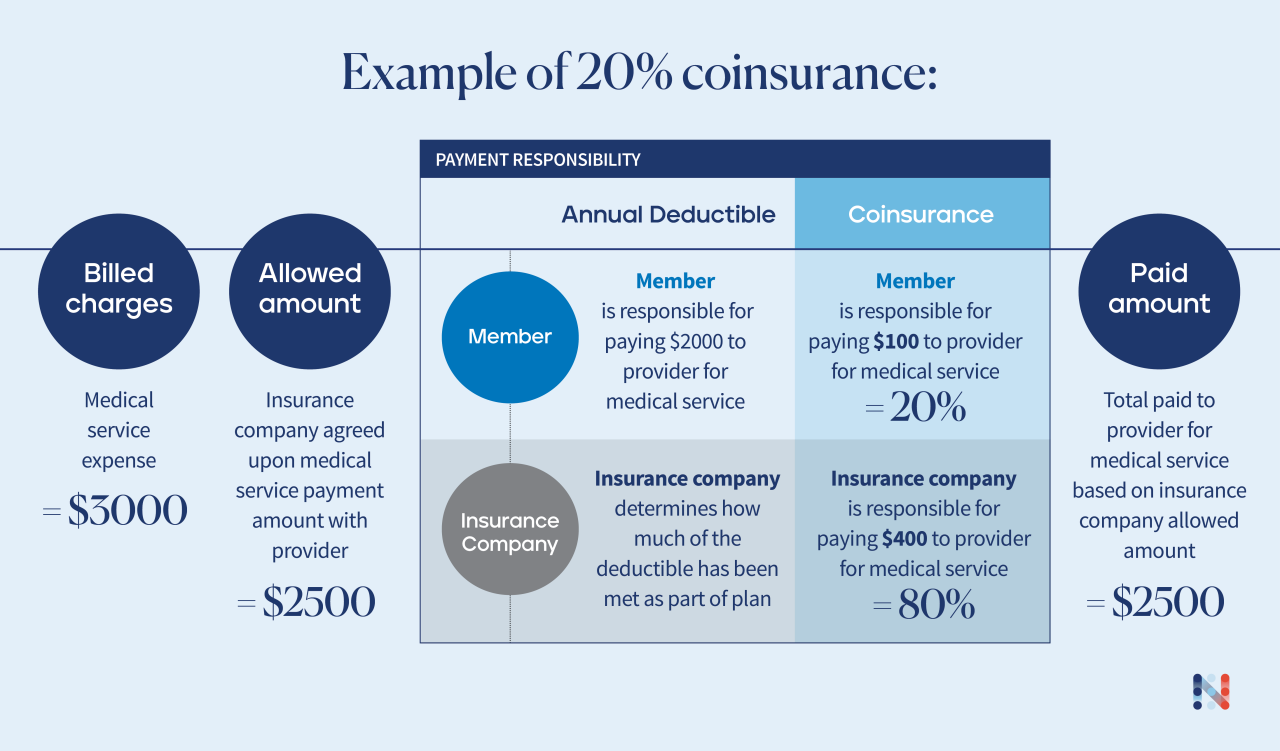

4. Coinsurance

A percentage you pay after deductible.

Example: Insurance pays 80%, you pay 20%

5. Out-of-Pocket Maximum

The most you will pay in a year.

After this, insurance pays 100%.

Example: $8,700/year (ACA cap for individuals)

How a Health Insurance Claim Works (Real Example)

Case: John — Office Worker, Illinois

Monthly premium: $420

Deductible: $2,500

Coinsurance: 20%

Out-of-pocket max: $8,000

John has surgery costing $20,000.

Cost Breakdown

| Step | Amount |

|---|---|

| Pays deductible | $2,500 |

| Remaining bill | $17,500 |

| Coinsurance (20%) | $3,500 |

| Total John pays | $6,000 |

| Insurance pays | $14,000 |

Without insurance: $20,000

With insurance: $6,000

Types of Health Insurance in the US

1. Employer-Sponsored Health Insurance

Most working Americans get insurance through their job.

✔ Employer pays part of premium

✔ Group rates are cheaper

✔ Coverage starts after joining

Best option if available.

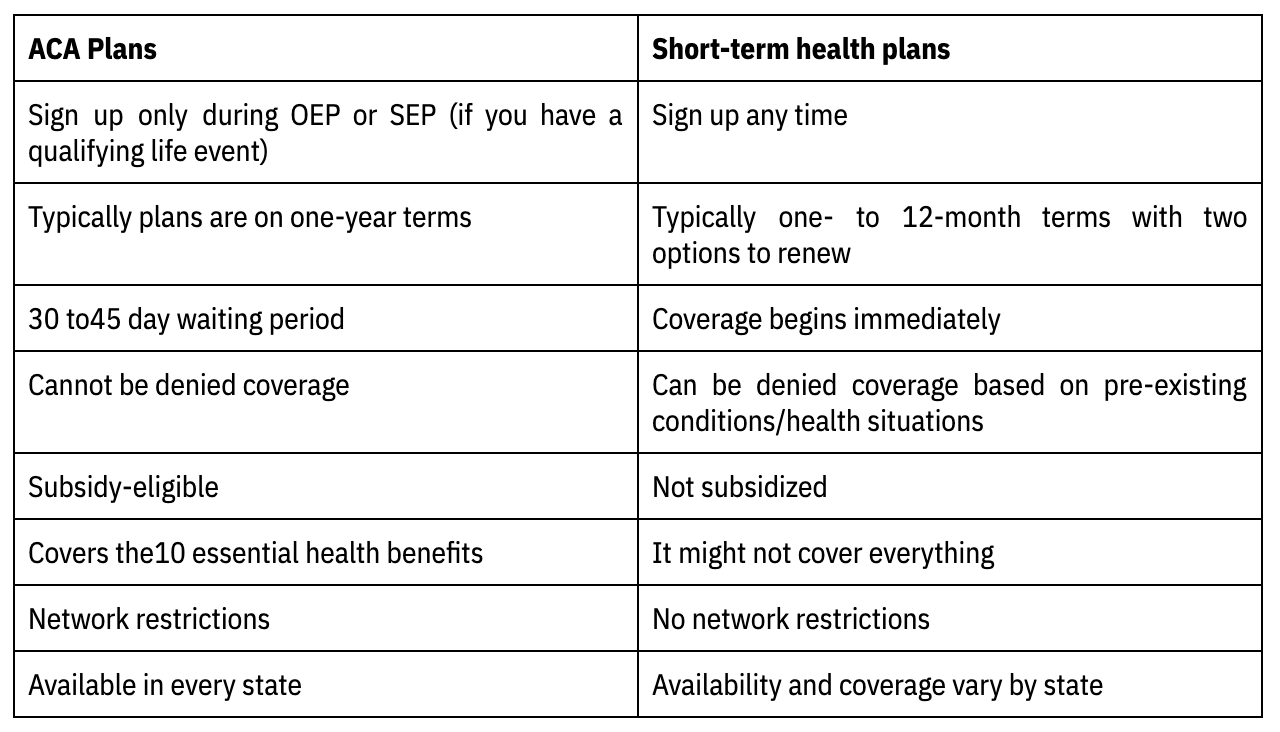

2. ACA / Marketplace Plans (HealthCare.gov)

If you don’t have job insurance, buy through ACA.

Benefits:

✔ Cannot deny for pre-existing conditions

✔ Income-based subsidies

✔ Standardized plans

Metal tiers:

| Plan | Monthly Cost | Best For |

|---|---|---|

| Bronze | Low | Rare doctor visits |

| Silver | Medium | Families |

| Gold | High | Chronic conditions |

| Platinum | Highest | Heavy care users |

3. Medicaid (Low-Income Coverage)

Run by states with federal support.

✔ Very low cost

✔ Covers millions

✔ Income limits apply

Eligibility varies by state.

4. Medicare (Age 65+ or Disabled)

Covers:

Part A: Hospital

Part B: Doctors

Part C: Medicare Advantage

Part D: Prescriptions

Managed by CMS.

In-Network vs Out-of-Network (Critical Rule)

Always check provider network.

| Type | Your Cost |

|---|---|

| In-network | Low |

| Out-of-network | Very high or not covered |

Many surprise bills come from ignoring this rule.

Explanation of Benefits (EOB) — Not a Bill

An EOB shows:

What provider charged

What insurance paid

What you may owe

Never ignore EOBs.

They help catch billing errors.

Common Health Insurance Mistakes Americans Make

❌ Choosing lowest premium only

❌ Ignoring deductible size

❌ Not checking doctor network

❌ Missing open enrollment

❌ Skipping insurance to save money

These mistakes cost thousands later.

How to Choose the Right Health Insurance Plan

Simple 5-Step Method

Check if employer plan exists

Estimate yearly doctor visits

Compare total yearly cost (not just premium)

Check prescriptions coverage

Confirm doctors are in-network

Cost Comparison Chart (Realistic Example)

Family of 3 — Texas

| Plan | Premium/Year | Max Cost |

|---|---|---|

| Bronze | $6,200 | $15,000 |

| Silver | $8,500 | $12,000 |

| Gold | $11,000 | $9,000 |

Gold costs more monthly but less overall if care is heavy.

Helpful Videos & Official Resources

Recommended Learning

Health Insurance Basics (HHS)

https://www.youtube.com/watch?v=Y3u0Z6yF0KkHow Deductibles Work

https://www.youtube.com/watch?v=5v5s8kT4mA0ACA Marketplace Explained

https://www.youtube.com/watch?v=4GZx3ZKzZ9IMedicare Explained Simply

https://www.youtube.com/watch?v=H5Zp3Z0m6jE

(Search official government channels for updates.)

Internal Links (MoneySense America)

👉 “Individual Health Insurance Explained in the US”

moneysenseamerica.blogspot.com👉 “How to Reduce Medical Bills in the USA”

moneysenseamerica.blogspot.com👉 “Emergency Fund Planning for US Families”

moneysenseamerica.blogspot.com

Frequently Asked Questions (FAQ)

Q1: Is health insurance mandatory in the US?

There is no federal penalty now, but some states require coverage.

Q2: Can I buy insurance anytime?

No. Only during open enrollment or special life events.

Q3: What is the cheapest plan?

Bronze plans have low premiums but high deductibles.

Q4: Does insurance cover all costs?

No. You still pay deductibles, copays, and coinsurance.

Q5: Is Medicaid better than ACA plans?

If eligible, Medicaid is usually cheaper.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute medical, legal, or financial advice. Health insurance laws, costs, and eligibility rules vary by state and change frequently. Always verify details through official government websites, licensed insurance agents, or qualified professionals. MoneySense America and the author are not responsible for actions taken based on this information.

Bibliography & References

U.S. Department of Health and Human Services

https://www.hhs.govCenters for Medicare & Medicaid Services

https://www.cms.govHealthCare.gov — ACA Marketplace

https://www.healthcare.govKaiser Family Foundation — Health Policy Data

https://www.kff.orgNational Institutes of Health — Healthcare Costs

https://www.nih.gov

Final Takeaway: The Golden Rule of US Health Insurance

Remember this:

🩺 Health insurance is not about avoiding doctors — it’s about avoiding financial disaster.

Choose based on total cost, not just monthly premium.

With the right plan, health insurance becomes a shield — not a burden.

Comments

Post a Comment