Health Insurance Deductibles in the US Explained: How They Work, Costs & Smart Saving Tips

Health Insurance Deductibles in the US Explained — A Simple Guide for Everyday Americans (2026)

Health Insurance Deductibles in the US Explained: How They Work, Costs & Smart Saving Tips

Learn what health insurance deductibles mean in the US. Understand costs, copays, coinsurance, real examples, and smart ways to lower medical bills legally.

“American family reviewing health insurance deductible and medical bills”

“Working adult checking deductible details online in the USA”

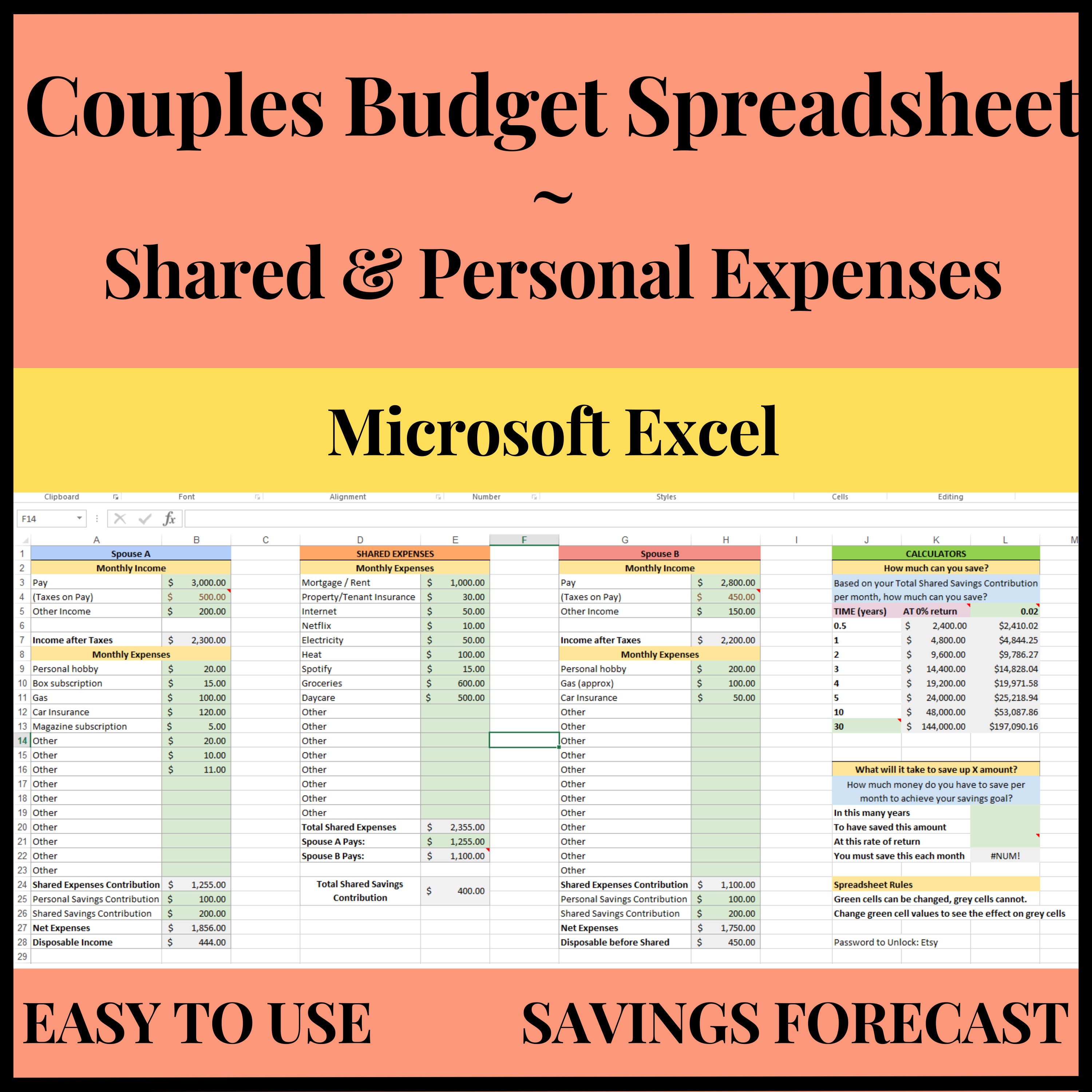

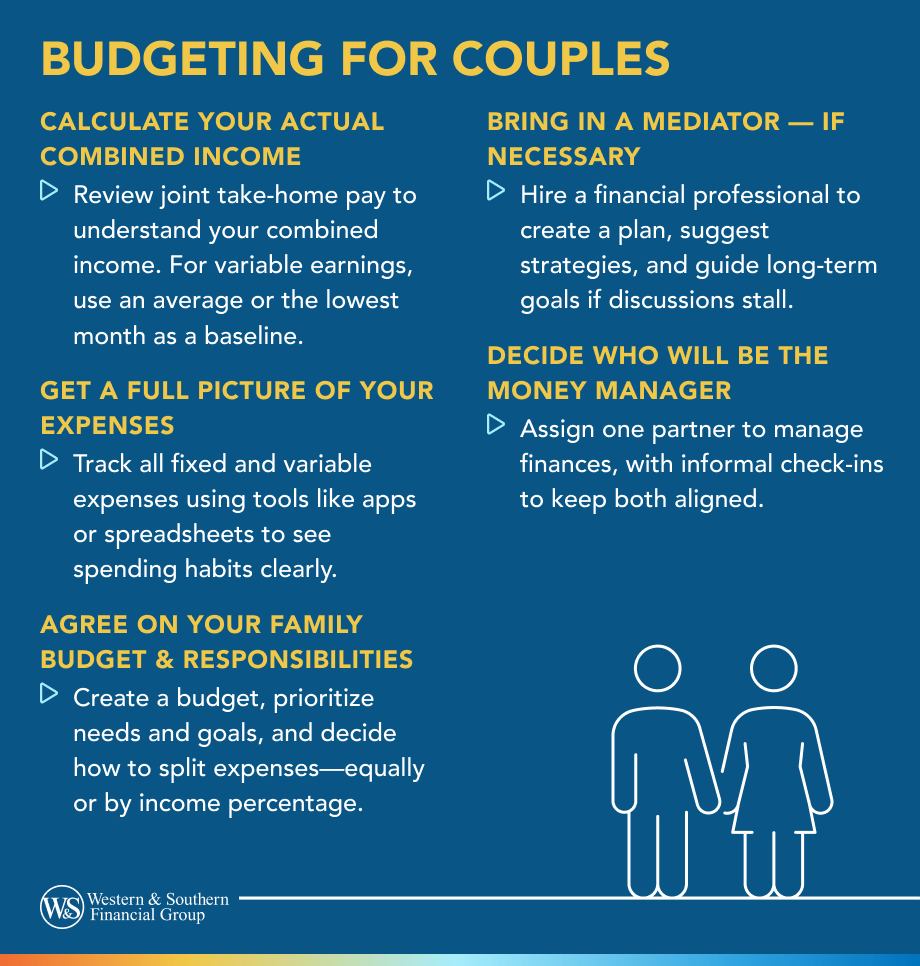

“Couple budgeting healthcare expenses with calculator”

“Explanation of Benefits showing deductible information”

“Family planning medical budget with insurance papers”

Health insurance in the United States can feel confusing.

People often say:

“I pay every month, but still get big hospital bills. Why?”

Most of the time, the answer is deductibles.

If you don’t understand how deductibles work, you may end up paying thousands of dollars more than expected.

This guide explains health insurance deductibles in simple words, with real US examples, charts, and practical tips.

Who Regulates Health Insurance in the US?

Health insurance rules are overseen by:

Centers for Medicare & Medicaid Services

Tax rules related to medical costs and subsidies are handled by:

Internal Revenue Service

These agencies make sure insurers follow national standards.

What Is a Health Insurance Deductible? (In Simple Words)

A deductible is:

The amount you must pay from your own pocket each year before your insurance starts paying most of your medical bills.

Example

If your deductible is $2,000, you must pay the first $2,000 of covered medical expenses yourself.

After that, insurance begins sharing costs.

Why Do Deductibles Exist?

Insurance companies use deductibles to:

✔ Reduce small claims

✔ Control premiums

✔ Encourage responsible use

In return, you get lower monthly premiums.

So, there is always a trade-off:

👉 Lower premium = Higher deductible

👉 Higher premium = Lower deductible

The 5 Key Cost Terms You Must Know

Understanding deductibles is easier when you know these five terms.

| Term | Meaning |

|---|---|

| Premium | Monthly payment |

| Deductible | What you pay first |

| Copay | Fixed visit fee |

| Coinsurance | Percentage you pay |

| Out-of-Pocket Max | Yearly spending limit |

Let’s explain them simply.

1️⃣ Premium

Your monthly bill to keep insurance active.

Example: $350/month

2️⃣ Deductible

What you pay before insurance helps.

Example: $2,500/year

3️⃣ Copay

A flat fee per visit.

Example: $25 doctor visit

4️⃣ Coinsurance

Your share after deductible.

Example: You pay 20%, insurance pays 80%

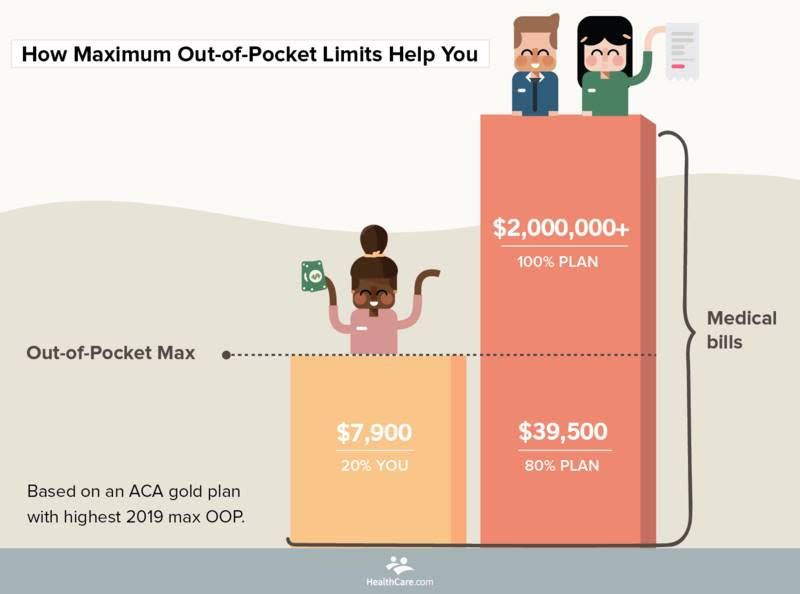

5️⃣ Out-of-Pocket Maximum

The most you’ll pay in a year.

After this, insurance pays 100%.

Example: $8,700/year

How Deductibles Work in Real Life (Step-by-Step)

Let’s see a real example.

Case: David — Warehouse Worker (Ohio)

Plan Details:

Premium: $280/month

Deductible: $3,000

Coinsurance: 20%

Out-of-pocket max: $8,000

Medical Bill: $12,000 (surgery)

Payment Breakdown

| Step | Amount |

|---|---|

| Deductible | $3,000 |

| Remaining bill | $9,000 |

| Coinsurance (20%) | $1,800 |

| David pays | $4,800 |

| Insurance pays | $7,200 |

Without insurance: $12,000

With insurance: $4,800

Low Deductible vs High Deductible Plans

Comparison Table

| Feature | Low Deductible | High Deductible |

|---|---|---|

| Premium | High | Low |

| Deductible | Low | High |

| Best For | Frequent care | Healthy adults |

| Risk | Low | Higher |

Example

| Plan Type | Monthly | Deductible |

|---|---|---|

| Low Deductible | $480 | $500 |

| High Deductible | $220 | $5,000 |

High deductible saves $3,120/year in premiums, but risks higher bills.

High Deductible Health Plans (HDHP) & HSA

Many Americans choose HDHPs with Health Savings Accounts (HSA).

Benefits

✔ Lower premiums

✔ Tax-deductible savings

✔ Tax-free medical spending

✔ Long-term investment option

Good for freelancers and young workers.

When Do You NOT Pay the Deductible?

Some services are free even before meeting deductible.

These are called preventive services.

Usually include:

✔ Annual checkups

✔ Vaccines

✔ Screenings

✔ Blood pressure tests

ACA rules require this coverage.

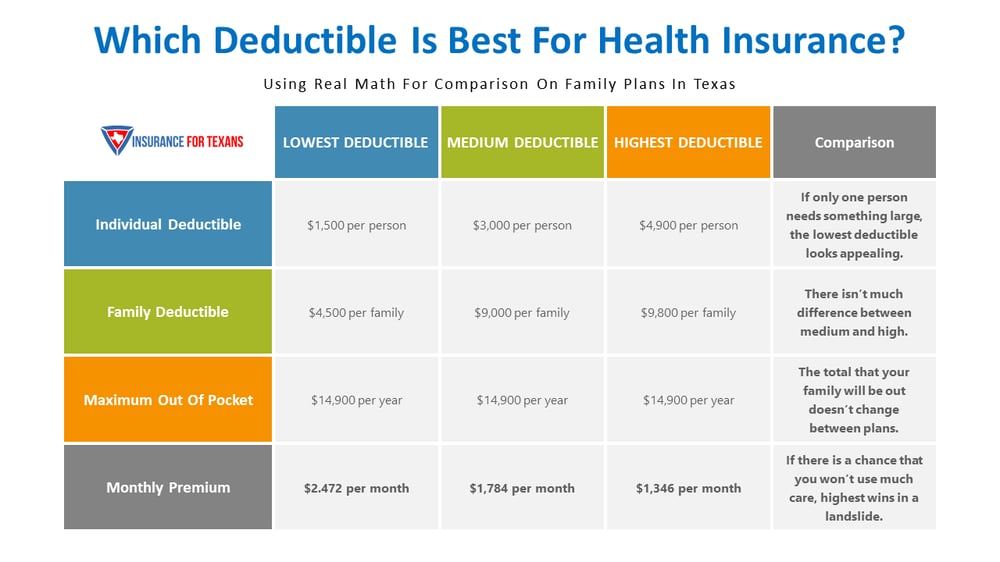

Individual vs Family Deductibles

Family plans have two deductibles:

Example

Family Plan:

Individual deductible: $3,000

Family deductible: $6,000

If one person hits $3,000 → insurance starts for them.

If whole family hits $6,000 → coverage begins for all.

Always check both numbers.

Deductibles in Different Plan Types

| Plan Type | Typical Deductible |

|---|---|

| HMO | Low–Medium |

| PPO | Medium–High |

| EPO | Medium |

| Bronze ACA | High |

| Gold ACA | Low |

Bronze plans usually have the highest deductibles.

Common Deductible Mistakes Americans Make

❌ Choosing cheapest premium only

❌ Ignoring deductible size

❌ Not reading EOB statements

❌ Using out-of-network doctors

❌ Forgetting yearly reset

Remember: Deductibles reset every year.

Cost Comparison Chart (Single Adult, Florida)

Annual Example

| Plan | Premium/Year | Deductible | Max Cost |

|---|---|---|---|

| Bronze | $3,600 | $6,500 | $9,000 |

| Silver | $5,400 | $2,800 | $8,500 |

| Gold | $8,400 | $900 | $6,000 |

Gold costs more monthly but protects you better.

How to Choose the Right Deductible (5-Step Method)

Step 1: Estimate Your Health Use

Rare visits → High deductible

Frequent care → Low deductible

Step 2: Check Emergency Savings

Have $5,000 saved?

High deductible may be safe.

No savings?

Choose lower deductible.

Step 3: Review Prescriptions

High drug costs → Lower deductible better.

Step 4: Compare Total Cost

Premium + Deductible = Real cost

Step 5: Check Network

Out-of-network bills ignore deductible rules.

Real-Life Case Study (USA)

Linda — Self-Employed Baker (Oregon)

Income: $46,000

Old Plan: Low deductible

Premium: $510/month

New Plan: HDHP + HSA

Premium: $240/month

Deductible: $4,000

Savings: $3,240/year

Used HSA for medical bills

Result: More control, less stress.

Internal Links (MoneySense America)

👉 “How Health Insurance Works in the US”

moneysenseamerica.blogspot.com👉 “Cheapest Health Insurance Plans in US”

moneysenseamerica.blogspot.com👉 “HMO vs PPO vs EPO Plans Explained”

moneysenseamerica.blogspot.com

Helpful Videos & Learning Resources

Recommended Viewing

How Deductibles Work

https://www.youtube.com/watch?v=5v5s8kT4mA0Health Insurance Basics

https://www.youtube.com/watch?v=Y3u0Z6yF0KkHDHP & HSA Explained

https://www.youtube.com/watch?v=8Zp6B2yF5cEUnderstanding EOB Statements

https://www.youtube.com/watch?v=H5Zp3Z0m6jE

(Search official channels for latest updates.)

Frequently Asked Questions (FAQ)

Q1: Do I pay deductible every month?

No. It is yearly, not monthly.

Q2: Does deductible reset?

Yes. Usually every January.

Q3: Do copays count toward deductible?

Sometimes. Check your plan.

Q4: Are prescriptions part of deductible?

Often yes, especially in HDHPs.

Q5: Is high deductible bad?

Not if you are healthy and have savings.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute medical, legal, or financial advice. Health insurance rules, deductible limits, and plan designs vary by state and insurer and may change. Always verify details through official government websites or licensed insurance professionals. MoneySense America and the author are not responsible for decisions made based on this content.

Bibliography & References

U.S. Department of Health and Human Services

https://www.hhs.govCenters for Medicare & Medicaid Services

https://www.cms.govHealthCare.gov — Insurance Costs

https://www.healthcare.govKaiser Family Foundation — Health Policy Data

https://www.kff.orgInternal Revenue Service — HSA Rules

https://www.irs.gov

Final Takeaway: Know Your Deductible, Control Your Costs

Remember this rule:

💡 Your deductible decides how painful a medical bill will feel.

Low deductible = safer but costly monthly

High deductible = risky but cheaper monthly

Choose based on your health, savings, and lifestyle.

When you understand deductibles, health insurance stops being confusing — and starts protecting your money.

Comments

Post a Comment