Debt Settlement vs Debt Consolidation in the USA — a clear, practical guide for working Americans

Debt Settlement vs Debt Consolidation in the USA — a clear, practical guide for working Americans

Quick summary: Debt consolidation combines debts into one loan or plan (you still pay what you owe). Debt settlement negotiates to reduce the amount you owe (you may pay less, but it has costs and tax consequences). This guide explains how each works, who should consider which option, costs, risks, steps to take, and real-world examples for U.S. middle-class working adults.

What they are — in plain words

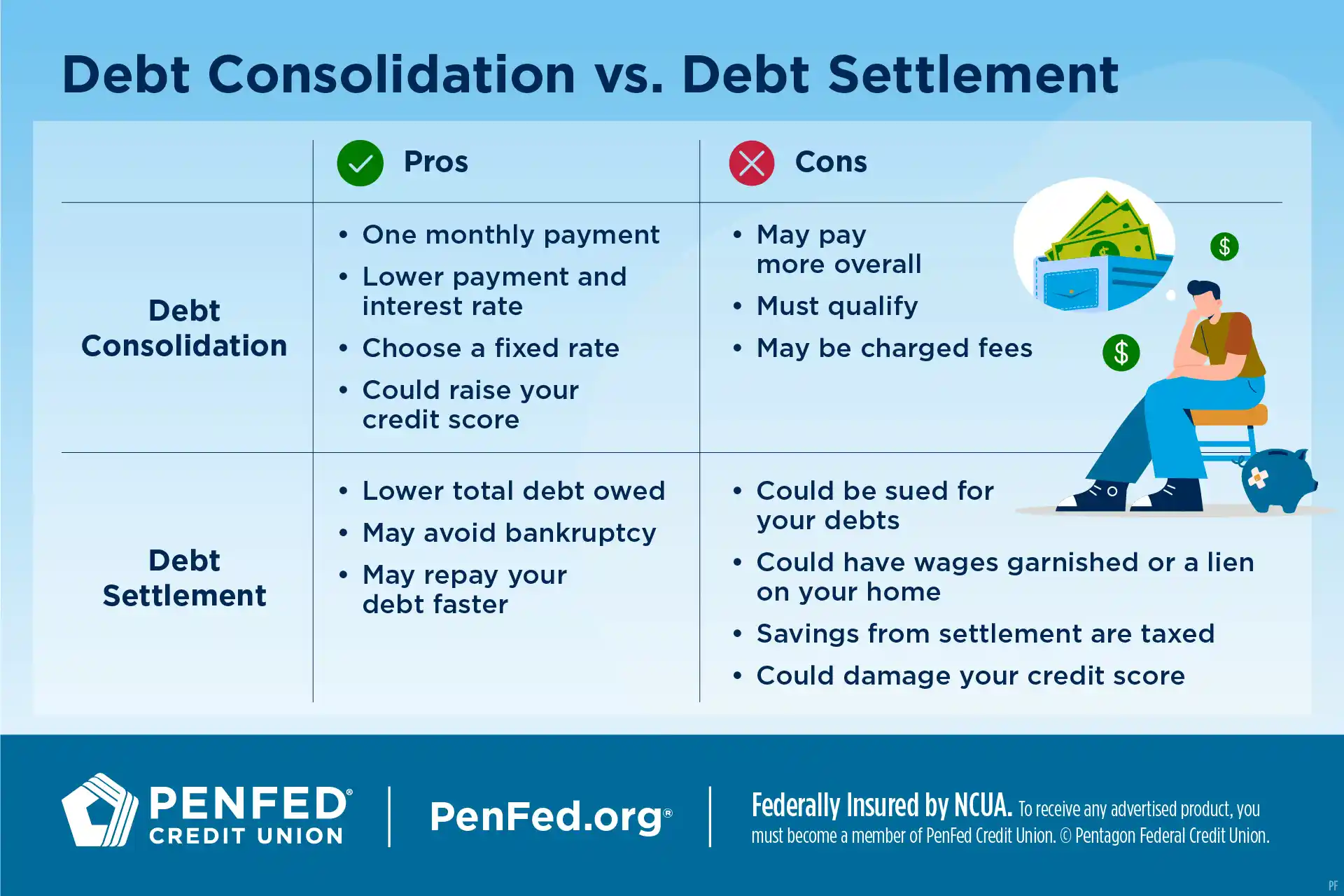

Debt consolidation: You take one new loan (or use a balance-transfer card, or a debt-management plan through a nonprofit credit counselor) to pay off multiple debts. You now have one payment, often at a lower interest rate or with simpler terms. Think: gathering loose papers into one neat folder. (Investopedia)

Debt settlement: You (or a settlement company) negotiate with creditors to accept less than what you owe. Often this happens after accounts become delinquent because creditors are more willing to accept a reduced lump-sum than little or no payments. Think: asking a lender to take a smaller check now instead of getting nothing later. (Consumer Financial Protection Bureau)

(If you want a one-line rule: consolidation aims to simplify and reduce interest; settlement aims to reduce principal.)

Who each option helps

Debt consolidation is usually best if:

You’re current or only slightly behind on payments.

You have steady income and can afford monthly payments.

You want to rebuild credit over time.

Example: You have $25,000 across cards at 18–24% APR, qualify for a 9% personal loan — consolidation lowers monthly interest and makes budgeting easier. (Investopedia)

Debt settlement may be considered if:

Your accounts are seriously past due or in collections.

You can save a lump sum to offer a creditor.

You accept the hit to your credit and possible tax bill.

Example: You owe $12,000 in unpaid credit cards; after negotiation you pay $6,500 total over time and avoid bankruptcy — but your credit score drops and you may receive a tax form. (Investopedia)

Costs — what you’ll actually pay

| Cost type | Debt consolidation | Debt settlement |

|---|---|---|

| Fees | Loan origination, closing, or monthly interest (varies) | Settlement company fees (commonly 15–25% of amount settled) or negotiation time if DIY. (Investopedia) |

| Interest | Usually lower overall if you get a lower-rate loan | You stop paying for a while (accrue late interest); settled debt may have no interest after agreement |

| Credit score | Can improve over time if payments are on time | Usually falls significantly during process, and marks remain for years |

| Taxes | No tax event | Forgiven amount may be taxable; expect Form 1099-C if $600+ forgiven. (irs.gov) |

Tip: Debt settlement companies are not allowed to charge huge upfront fees before settling debts. Federal rules and consumer protections exist — check the [CFPB] guidance when choosing a provider. (Consumer Financial Protection Bureau)

(Entities: IRS, Consumer Financial Protection Bureau, Investopedia)

Credit and tax effects — plain facts

Credit: Consolidation can help your score over time (lower utilization, consistent payments). Settlement usually causes a sharp drop: late payments, charge-offs, and “settled for less” notations can stay on reports up to 7 years. (Investopedia)

Taxes: If a creditor forgives part of your debt, the IRS generally treats that forgiven amount as taxable income. You may receive a Form 1099-C if $600 or more is canceled—plan for a potential tax bill or qualify for exceptions (insolvency, bankruptcy, qualified principal residence exclusions). Always consult tax pros about your situation. (irs.gov)

Risks and red flags (watch out)

Settlement companies that tell you to stop paying creditors immediately and promise guaranteed results — be skeptical. Stopping payments damages credit and can lead to lawsuits. (Consumer Financial Protection Bureau)

Upfront fees or pressure to sign quickly — federal law generally prohibits certain fee structures for debt relief. Check for nonprofit credit counselors (NFCC) and review CFPB resources. (Consumer Financial Protection Bureau)

Tax surprises after settlement — never assume forgiven debt isn’t taxable. Keep records and ask for a settlement letter stating the forgiven amount. (irs.gov)

A simple decision flow (diagram)

Are you current or only a little behind? → Consolidation (look for low-rate personal loans or credit-union offers).

Seriously behind or in collections? → Consider settlement only after exploring credit counseling and bankruptcy alternatives.

Can you save a lump sum? → Settlement more likely to work.

Worried about taxes? → Get tax advice before finalizing settlement.

Steps to take today (practical checklist)

Get your numbers: total balances, APRs, minimum payments. Pull your credit report.

Talk to a nonprofit credit counselor (National Foundation for Credit Counseling or local credit union). They can show consolidation and debt management options. (Investopedia)

Compare consolidation offers: personal loan, balance transfer card, or DMP. Check APR, term, fees.

If considering settlement: try DIY before paying a company. Save in a separate account for lump-sum offers. Only use reputable firms; keep all agreements in writing. (Investopedia)

Talk to a tax advisor about possible Form 1099-C and insolvency exceptions. (irs.gov)

Short case studies (realistic examples)

Maria, single parent, steady job — $18,000 credit card debt at 22% APR. She qualifies for a credit-union consolidation loan at 9% APR. Her monthly payment drops and she slowly rebuilds credit through on-time payments. (Consolidation win.)

James, laid off, two cards charged off — owes $14,000, no steady income. He negotiates settlements on delinquent accounts and pays $7,000 over 18 months. He receives a 1099-C for $3,500 forgiven. He pays some tax but avoids bankruptcy. (Settlement with tax and credit costs.)

FAQ — short and clear

Q: Will consolidation erase my debt?

A: No. It combines or replaces debts with a new loan or plan. You still repay principal and interest. (Investopedia)

Q: Is settled debt taxable?

A: Often yes. Forgiven amounts are generally taxable; watch for Form 1099-C and consult a tax advisor. (irs.gov)

Q: Can consolidation hurt my credit?

A: It can temporarily (hard credit check) but often helps over time if payments are made. (Investopedia)

Q: Are debt settlement companies scams?

A: Not always, but scams exist. Look for red flags: upfront fees, promises to stop calls instantly, or guarantees. Use CFPB resources and check BBB ratings. (Consumer Financial Protection Bureau)

Recommended resources & videos

CFPB guide on debt relief and differences between counseling, consolidation and settlement. (Consumer Financial Protection Bureau)

IRS Topic on canceled debt and Form 1099-C. (irs.gov)

Investopedia’s comparison and fee breakdown for settlement vs consolidation. (Investopedia)

Suggested watch: Search YouTube for “debt consolidation vs debt settlement CFPB” for clear agency videos and consumer stories (look for official CFPB channel content).

Internal links (read next on MoneySense America)

“How to Choose a Personal Loan: Rate, Term, and Fees” — practical steps to compare consolidation loans. (Internal link) moneysenseamerica.blogspot.com

“Credit Repair Basics After Debt Trouble” — what to do to rebuild credit after settlement or collections. (Internal link)

(Add these posts to your blog if not already present — they pair well with this guide.)

Statutory disclaimer

This article is for educational purposes only. It is not legal, tax, or financial advice. Laws and tax rules change — consult a licensed tax professional, attorney, or certified financial counselor for advice tailored to your situation. The author and MoneySense America accept no liability for actions taken based on this article.

Bibliography & sources (selected)

Consumer Financial Protection Bureau — difference between credit counseling, debt settlement, and debt consolidation. (Consumer Financial Protection Bureau)

IRS — About Form 1099-C, Cancellation of Debt; Topic No. 431 Canceled Debt. (irs.gov)

Investopedia — difference between debt consolidation and settlement; fee data. (Investopedia)

NASDAQ article on debt settlement costs and industry trends. (Nasdaq)

Final takeaway — a quick checklist to decide right now

Are you current or slightly behind and want to protect credit? → Explore consolidation.

Are you deep in delinquency, can save a lump sum, and accept credit/tax costs? → Consider settlement, after consulting tax/counseling pros.

Unsure? Talk to a nonprofit credit counselor first — low cost, unbiased options often exist. (Investopedia)

Comments

Post a Comment