Cheapest Health Insurance Plans in the US (2026): Low-Cost Options, Subsidies & Money-Saving Tips

Cheapest Health Insurance Plans in the US — A Simple Guide for Smart Savings (2026)

Cheapest Health Insurance Plans in the US (2026): Low-Cost Options, Subsidies & Money-Saving Tips

Discover the cheapest health insurance plans in the US. Learn about ACA Bronze plans, Medicaid, subsidies, HSAs, and real examples to lower your healthcare costs legally.

“American family reviewing affordable health insurance options at home”

“Working adult comparing cheapest health insurance plans online in the USA”

“Couple budgeting medical expenses with health insurance documents”

“HealthCare.gov marketplace website on laptop screen”

“Family planning low-cost health coverage in America”

Health insurance in the US can feel expensive, confusing, and stressful.

Many people ask:

“Is there any good health insurance that I can actually afford?”

The honest answer is:

👉 Yes. But you need to know where to look and how to compare.

With the right plan, many Americans pay under $100 per month — sometimes even $0.

This guide explains, in simple words, how to find the cheapest health insurance plans in the US, who qualifies, and how to save thousands every year.

Who Regulates Health Insurance in the US?

Health insurance rules are set and monitored by:

Centers for Medicare & Medicaid Services

Most low-cost individual plans are sold through HealthCare.gov under the Affordable Care Act (ACA).

Tax-related subsidies are managed by the

Internal Revenue Service.

Understanding this system helps you find the cheapest legal plans.

The 4 Cheapest Health Insurance Options in the USA

Let’s look at the most affordable choices for everyday Americans.

1️⃣ ACA Bronze Plans — Cheapest Marketplace Option

For most self-employed people, freelancers, and workers without job coverage, ACA Bronze plans are the cheapest legal insurance.

Why Bronze Plans Are Cheap

✔ Lowest monthly premiums

✔ Available in every state

✔ Eligible for subsidies

✔ Covers emergencies and basics

How They Work

| Feature | Bronze Plan |

|---|---|

| Premium | Low |

| Deductible | High |

| Copays | Moderate |

| Best For | Healthy adults |

Example: Retail Worker (Arizona)

Income: $34,000/year

Single, age 28

Bronze plan cost:

Without subsidy: $390/month

With subsidy: $95/month

Annual savings: $3,540

2️⃣ Medicaid — The Cheapest (Often $0)

If your income is low, Medicaid is usually the cheapest option.

✔ $0 or very low premium

✔ Very low copays

✔ Strong coverage

✔ Covers prescriptions

Who Qualifies?

Eligibility depends on state and income.

Example (Medicaid expansion states):

| Household Size | Max Income (Approx.) |

|---|---|

| 1 Person | $20,000 |

| 2 People | $27,000 |

| 3 People | $34,000 |

Many gig workers qualify in slow business years.

Always check eligibility.

3️⃣ Silver Plans with Cost-Sharing Reductions (CSR)

If your income is moderate, Silver plans can be cheaper in practice than Bronze.

Why?

Because of Cost-Sharing Reductions (CSR).

What CSR Does

✔ Lowers deductible

✔ Reduces copays

✔ Cuts out-of-pocket max

Only available on Silver plans.

Example: Delivery Driver (Georgia)

Income: $28,000

Family size: 2

Silver + CSR:

Premium: $120/month

Deductible: $700

Bronze:

Premium: $90/month

Deductible: $7,000

👉 Silver is cheaper when medical care is needed.

4️⃣ Employer-Sponsored Low-Cost Plans

If your job offers insurance, this is often the cheapest route.

✔ Employer pays part of premium

✔ Group discounts

✔ Lower deductibles

Example:

Warehouse worker in Ohio:

Employer plan: $85/month

ACA Bronze: $210/month

Employer plan wins.

Always compare.

Understanding the Real Cost (Not Just Premium)

Many people choose the cheapest premium and regret it later.

You must look at total yearly cost.

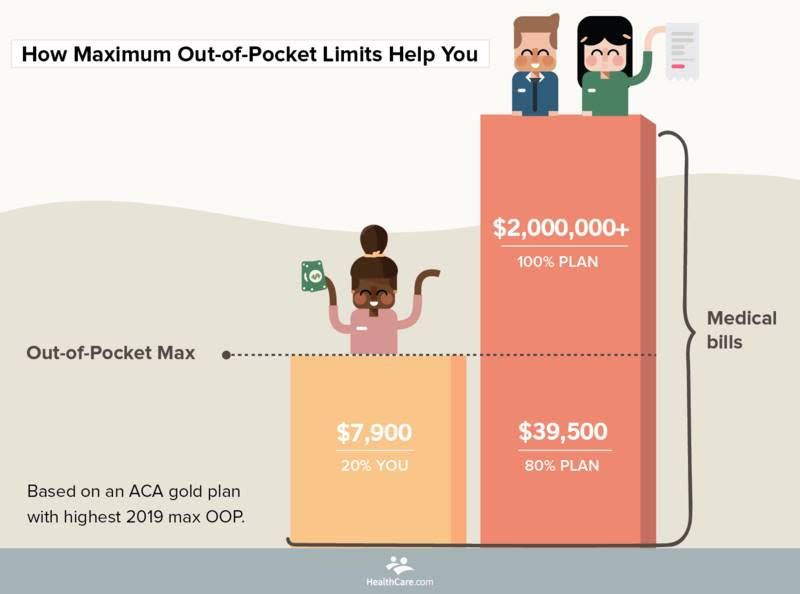

5 Important Cost Terms

| Term | Meaning |

|---|---|

| Premium | Monthly payment |

| Deductible | Pay before insurance helps |

| Copay | Fixed visit cost |

| Coinsurance | % you pay after deductible |

| Out-of-Pocket Max | Yearly limit |

Example: Construction Worker (Texas)

Plan: Bronze

Premium: $110/month

Deductible: $6,500

Out-of-pocket max: $9,000

Hospital bill: $12,000

You pay:

$6,500 deductible

coinsurance = $1,200

Total: $7,700

Insurance saves: $4,300

Cheapest Plans by Income Level (Chart)

Single Adult Example

| Annual Income | Best Cheap Option | Avg Monthly Cost |

|---|---|---|

| Under $20k | Medicaid | $0 |

| $25k–$35k | Silver + CSR | $80–$140 |

| $35k–$55k | Bronze + Subsidy | $90–$200 |

| $60k+ | Bronze/Employer | $200–$350 |

Your income decides your best deal.

How ACA Subsidies Reduce Your Premium

Subsidies are based on estimated yearly income.

Lower income = higher discount.

Example Subsidy Impact

| Income | Bronze Premium |

|---|---|

| $28,000 | $75 |

| $40,000 | $150 |

| $55,000 | $260 |

Important: Report income changes quickly to avoid tax problems.

Cheapest Strategy for Healthy Adults: Bronze + HSA

If you’re healthy, choose:

✔ High Deductible Bronze Plan

✔ Open Health Savings Account (HSA)

Benefits:

Tax deduction

Tax-free medical spending

Long-term savings

Great for freelancers and young workers.

Common Mistakes That Make Insurance Expensive

❌ Skipping subsidies

❌ Missing enrollment deadline

❌ Choosing lowest premium blindly

❌ Using out-of-network doctors

❌ Not updating income

These mistakes cost thousands.

How to Find the Cheapest Plan (5-Step Method)

Check Medicaid eligibility

Compare ACA plans on HealthCare.gov

Estimate yearly doctor visits

Compare “Total Cost,” not just premium

Confirm doctor network

Repeat every year.

Real-Life Case Study (USA)

Carlos — Rideshare Driver (Nevada)

Income: $31,000

Single

Old plan: Off-market private plan

Cost: $420/month

New strategy:

✔ Switched to ACA Silver + CSR

✔ Updated income

New cost: $105/month

Saved: $3,780/year

Helpful Videos & Official Resources

Recommended Learning

ACA Marketplace Explained

https://www.youtube.com/watch?v=4GZx3ZKzZ9IHow Deductibles Work

https://www.youtube.com/watch?v=5v5s8kT4mA0Medicaid Eligibility Guide

https://www.youtube.com/watch?v=Y3u0Z6yF0KkHealth Insurance Basics

https://www.youtube.com/watch?v=H5Zp3Z0m6jE

(Search official government channels for updates.)

Internal Links (MoneySense America)

👉 “How Health Insurance Works in the US”

moneysenseamerica.blogspot.com👉 “Best Health Insurance for Self-Employed in the US”

moneysenseamerica.blogspot.com👉 “How to Reduce Medical Bills in the USA”

moneysenseamerica.blogspot.com

Frequently Asked Questions (FAQ)

Q1: What is the cheapest health insurance in the US?

Medicaid is usually cheapest. Otherwise, subsidized ACA Bronze or Silver plans.

Q2: Can I get insurance for under $50/month?

Yes, with strong subsidies or Medicaid.

Q3: Are off-market plans cheaper?

Sometimes monthly, but often risky and limited.

Q4: Can I buy anytime?

No. Only during Open Enrollment or Special Enrollment.

Q5: Do cheap plans cover emergencies?

Yes, ACA plans must cover emergencies.

Statutory Disclaimer

This article is for educational and informational purposes only. It does not constitute medical, legal, or financial advice. Health insurance laws, pricing, and eligibility rules vary by state and change frequently. Always verify information through official government websites or consult a licensed insurance professional. MoneySense America and the author are not responsible for decisions made based on this content.

Bibliography & References

U.S. Department of Health and Human Services

https://www.hhs.govCenters for Medicare & Medicaid Services

https://www.cms.govHealthCare.gov Marketplace

https://www.healthcare.govKaiser Family Foundation (KFF) — Health Data

https://www.kff.orgInternal Revenue Service — ACA Tax Credits

https://www.irs.gov

Final Takeaway: Cheap Can Still Be Smart

Remember this rule:

💡 The cheapest plan is the one with the lowest total yearly cost — not just the lowest premium.

Use subsidies.

Compare carefully.

Review every year.

With the right choice, affordable health insurance is possible in America.

Comments

Post a Comment