Best Health Insurance for Self-Employed in the US (2026 Guide): ACA Plans, Costs, Subsidies & Smart Tips

Best Health Insurance for Self-Employed in the US — A Practical Guide for 2026

Best Health Insurance for Self-Employed in the US (2026 Guide): ACA Plans, Costs, Subsidies & Smart Tips

Self-employed in the US? Learn the best health insurance options, ACA marketplace plans, subsidies, HSAs, Medicaid, and cost comparisons with real examples.

“Self-employed freelancer reviewing health insurance options in the USA”

“Small business owner comparing ACA marketplace plans online”

“Independent contractor budgeting medical insurance costs”

“Entrepreneur planning healthcare expenses at home office”

“Remote worker searching affordable health insurance USA”

Being self-employed in America gives freedom.

You choose your clients.

You set your hours.

You build your own income.

But there is one big responsibility:

You must buy your own health insurance.

No employer plan.

No HR department.

No company contribution.

In this guide, we explain — in clear, simple words — the best health insurance options for self-employed Americans, how much they cost, how to save money, and which plan may fit your situation.

Why Health Insurance Is Essential When You Work for Yourself

Medical costs in the US can be extremely high.

| Service | Average Cost Without Insurance |

|---|---|

| ER visit | $1,500+ |

| Broken bone | $3,000–$8,000 |

| Childbirth | $10,000–$20,000 |

| 3-day hospital stay | $30,000+ |

Without insurance, one accident can destroy savings.

Health insurance protects your income and your business.

Who Regulates Health Insurance in the US?

Health coverage laws are overseen by:

Centers for Medicare & Medicaid Services

Most individual plans are sold through the Affordable Care Act marketplace at HealthCare.gov.

Main Health Insurance Options for Self-Employed Americans

Let’s explore the best choices.

1️⃣ ACA Marketplace Plans (Most Common & Recommended)

The ACA (Affordable Care Act) marketplace is the top option for freelancers, contractors, gig workers, and entrepreneurs.

Why ACA Plans Are Popular

✔ Cannot deny pre-existing conditions

✔ Income-based subsidies

✔ Standard coverage rules

✔ Caps on out-of-pocket costs

Plans come in four levels:

| Plan | Monthly Premium | Best For |

|---|---|---|

| Bronze | Lowest | Rare doctor visits |

| Silver | Moderate | Most families |

| Gold | Higher | Frequent medical needs |

| Platinum | Highest | Heavy medical use |

Real Example: Freelance Designer (California)

Income: $52,000/year

Family: Single

Without subsidy → $520/month

With subsidy → $290/month

Silver plan deductible: $2,800

Out-of-pocket max: $8,000

Savings from subsidy: $2,760/year

2️⃣ Medicaid (If Income Is Lower)

If your income drops in a slow business year, you may qualify for Medicaid.

✔ Very low or no premium

✔ Comprehensive coverage

✔ State-based eligibility

Income limits vary by state.

Check eligibility at your state’s Medicaid website.

3️⃣ Health Sharing Ministries (Use With Caution)

Some self-employed individuals choose religious health sharing groups.

Pros:

Lower monthly cost

Cons:

Not insurance

Claims may not be guaranteed

Pre-existing conditions often excluded

Use carefully.

4️⃣ Short-Term Health Insurance

Temporary coverage (3–12 months).

✔ Cheaper

❌ Limited coverage

❌ No ACA protections

Best for short gaps only.

5️⃣ Spouse’s Employer Plan

If your spouse works full-time, joining their employer plan is often cheapest.

✔ Employer contributes

✔ Lower premiums

✔ Better network access

Always compare this option.

Understanding the Real Costs (Simple Breakdown)

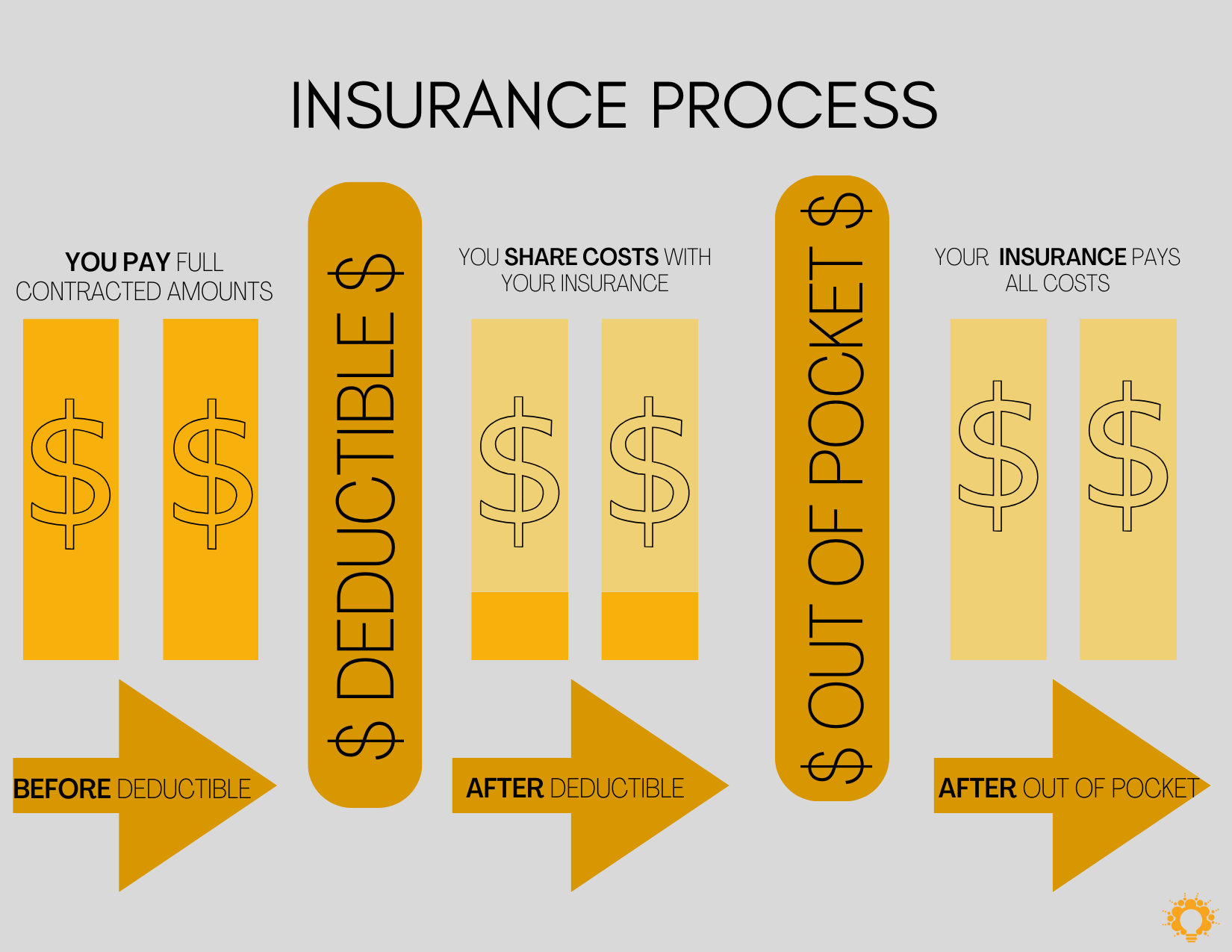

Key Cost Terms

| Term | Meaning |

|---|---|

| Premium | Monthly payment |

| Deductible | Amount you pay before insurance pays |

| Copay | Fixed cost per visit |

| Coinsurance | Percentage after deductible |

| Out-of-Pocket Max | Maximum yearly spending |

Example: Self-Employed Contractor (Texas)

Plan: Silver

Premium: $340/month

Deductible: $3,000

Coinsurance: 20%

Out-of-pocket max: $8,500

Hospital bill: $15,000

You pay:

First $3,000 deductible

20% of remaining $12,000 = $2,400

Total: $5,400

Without insurance: $15,000

Insurance saved: $9,600

How Subsidies Work for Self-Employed

ACA subsidies depend on estimated annual income.

Lower income = higher subsidy.

Example:

| Income | Estimated Monthly Premium (Silver) |

|---|---|

| $35,000 | $150 |

| $55,000 | $320 |

| $80,000 | $480 |

Important: You must estimate income carefully to avoid tax repayment later.

Tax rules are managed by the

Internal Revenue Service.

HSA: Smart Tax Tool for Self-Employed

If you choose a High Deductible Health Plan (HDHP), you can open a Health Savings Account (HSA).

Benefits:

✔ Tax-deductible contributions

✔ Tax-free growth

✔ Tax-free medical withdrawals

Great for healthy entrepreneurs.

How to Choose the Best Plan (Simple 5-Step Method)

Estimate yearly income accurately

Check ACA marketplace first

Compare total yearly cost (not just premium)

Confirm your doctors are in-network

Check prescription coverage

Cost Comparison Chart (Single Freelancer, Florida)

| Plan | Annual Premium | Max Out-of-Pocket | Best For |

|---|---|---|---|

| Bronze | $4,200 | $9,000 | Rare visits |

| Silver | $6,000 | $8,500 | Balanced coverage |

| Gold | $9,500 | $6,000 | Ongoing medical needs |

Choose based on expected usage.

Common Mistakes Self-Employed People Make

❌ Choosing cheapest premium only

❌ Underestimating income for subsidy

❌ Ignoring network restrictions

❌ Missing open enrollment

❌ Not reviewing plan yearly

These errors cost thousands.

Helpful Videos & Official Resources

ACA Marketplace Explained

https://www.youtube.com/watch?v=4GZx3ZKzZ9IHow Deductibles Work

https://www.youtube.com/watch?v=5v5s8kT4mA0Understanding Health Insurance Basics

https://www.youtube.com/watch?v=Y3u0Z6yF0KkHSAs Explained

https://www.youtube.com/watch?v=8Zp6B2yF5cE

(Search official government sources for updates.)

Internal Links (MoneySense America)

👉 “How Health Insurance Works in the US”

moneysenseamerica.blogspot.com👉 “Emergency Fund Planning for US Families”

moneysenseamerica.blogspot.com👉 “How to Reduce Medical Bills in the USA”

moneysenseamerica.blogspot.com

Frequently Asked Questions (FAQ)

Q1: Is ACA the best option for self-employed?

For most Americans, yes — because of subsidies and legal protections.

Q2: Can I deduct health insurance premiums?

Yes. Self-employed individuals can often deduct premiums on taxes.

Q3: What if my income changes mid-year?

Update your marketplace account immediately to adjust subsidies.

Q4: Is short-term insurance safe?

Only for temporary gaps.

Q5: What is the cheapest option?

Medicaid (if eligible). Otherwise, subsidized ACA Bronze.

Statutory Disclaimer

This article is for educational purposes only. It does not constitute legal, medical, or financial advice. Health insurance laws, subsidy rules, and eligibility requirements vary by state and change frequently. Always verify information through official government websites or consult a licensed insurance professional. MoneySense America and the author are not responsible for decisions made based on this content.

Bibliography & References

U.S. Department of Health and Human Services

https://www.hhs.govCenters for Medicare & Medicaid Services

https://www.cms.govHealthCare.gov Marketplace

https://www.healthcare.govKaiser Family Foundation — Health Data

https://www.kff.orgInternal Revenue Service — Health Insurance Tax Rules

https://www.irs.gov

Final Takeaway: Protect Your Health, Protect Your Business

If you are self-employed, remember:

💡 Your health is your income engine.

The best plan is not always the cheapest — it is the one that protects you from financial disaster.

Compare carefully.

Estimate income honestly.

Review yearly.

With smart planning, health insurance becomes protection — not pressure.

Comments

Post a Comment